What is bank linking? How it works and why it matters for payments

Data

March 25, 2026

|

Nick Rudy

Bank linking enables apps to connect to user bank accounts for secure data sharing and payment initiation.

If you’ve ever topped up a wallet, paid using your bank account, or connected your bank to a financial product, you’ve used bank linking.

It’s one of the most common (and important) steps in modern personal finance and fintech experiences.

For businesses, bank linking is what makes it possible to:

In this article, we’ll break down what bank linking is, how it works, and what to consider if you’re connecting banks for payments.

Bank linking is the process of connecting a user’s financial account to an application to access account information or move money.

Once a bank account is linked, that connection can be used to:

There are a few different ways to connect an external bank account, each with its own tradeoffs in speed, reliability, and user experience. We’ll break those down next.

There are a few common ways to connect an external bank account. While they may look similar on the surface, each creates a different type of connection depending on the authentication, security measures, and infrastructure used.

Users enter their account number and routing numbers directly.

This method does not create a true connection to the bank. It simply captures static details that can be used later for payments.

Tradeoffs:

After entering bank details, users verify ownership by confirming two small deposits sent to their account.

This adds a layer of validation, but it happens after a delay rather than in real time.

Tradeoffs:

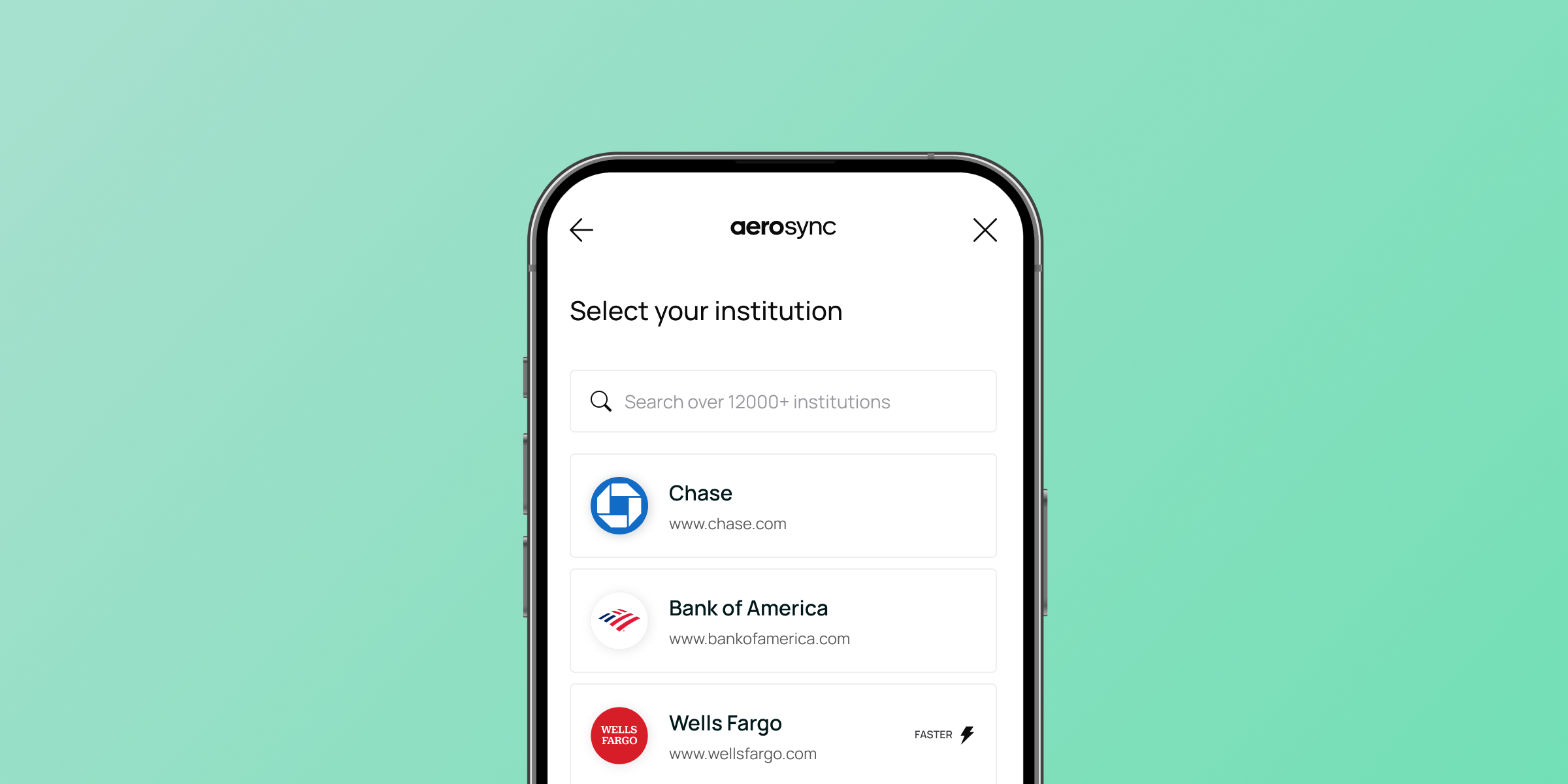

Users select their bank and log in through a third-party flow to connect their account instantly using their login information through online banking.

Behind the scenes, providers use a mix of methods. Some rely on direct bank APIs, while others use credential-based access, often referred to as screen scraping, where data is retrieved from a bank’s website.

These connections rely on industry standards and encryption protocols like transport layer security to protect sensitive data.

While these approaches can look similar to users, they can differ significantly in reliability, security, and how well they support payments.

Tradeoffs:

In API-based flows, authentication happens directly via online banking, typically in the customer's mobile app, where users grant permission to connect their bank for payments.

These open API connections create a structured, bank-authorized link instead of relying on static data or shared credentials.

As part of this process, users typically complete multi-factor authentication (MFA) through their bank. This can include receiving a one-time code via email or phone number, using biometrics, or confirming the login within their banking app.

Tradeoffs:

.png)

Bank linking has a direct, measurable impact on how your payments perform.

The way a bank account is connected influences how many users complete the flow, how many payments go through, and what those payments actually cost your business.

To evaluate performance, it helps to track conversion, payment success, and cost per payment.

How many users connect successfully?

This measures how many users complete the bank linking flow.

If users drop off at this step, they never reach payment. That translates directly into lost transactions.

What percentage of initiated payments go through?

A successful connection does not guarantee a successful payment.

This metric reflects how reliable your bank connections are once money starts moving.

What does each completed payment cost?

This metric captures the impact of failed payments, retries, and operational overhead, giving you a clear picture of how bank payments (and the pricing associated with their infrastructure) affect your margins as you scale. For businesses using bank payments to lower payment processing costs, it's important to track the associated cost per successful bank connection as these charges can increase total payment costs.

As more businesses rely on bank payments, expectations around bank linking are changing across finance apps and digital personal finance products.

Teams are placing more emphasis on whether a connection can actually support a payment in the moment it matters.

That shift is driving a move toward more modern approach that includes:

Many implementations now rely on API-based connections that link accounts directly through a user’s bank.

These connections are:

There is also a growing focus on verifying account details earlier in the process.

Instead of discovering issues after a failed payment, businesses can:

Teams are also improving the user experience around bank linking.

The goal is to: