Why pay by bank feels natural to Gen Z and younger millennials

Payments

February 18, 2026

|

Nate Sousa

Nate writes content for Aeropay. His mission is to make pay by bank clearer and easier to understand for everyone.

Digital experiences have reshaped how everyone expects things to work. From the apps people use to shop and stream to how they text and manage money, interactions are designed to feel instantaneous, intuitive, and clear. When something feels slow or confusing, it stands out immediately.

That same lens already applies at checkout. Consumers increasingly judge payment experiences the way they judge any other digital interaction. Intuitively, they’re asking whether it feels straightforward, whether they’re confident the transaction worked, and how quickly they receive confirmation. Research on how consumers interact with payments shows that trust, clarity, and ease of use now play a central role in how payment experiences are evaluated.

There’s no group this is more true for than Gen Z and younger millennials, who grew up in a mobile-first world. For them, moving money through connected accounts is routine. Managing spending, transferring funds, investing, gaming, earning rewards—it all happens through tools designed to feel immediate and clear.

That’s the standard they’re used to.

Those same expectations extend into every digital interaction. Younger consumers apply them when ordering a coffee, subscribing to a service, or completing a purchase online. As a result, payment experiences aren’t evaluated in a vacuum anymore. They shape how customers perceive the brands behind them.

That alignment is exactly why pay by bank feels increasingly natural to Gen Z and younger millennials and why it signals where checkout is heading next.

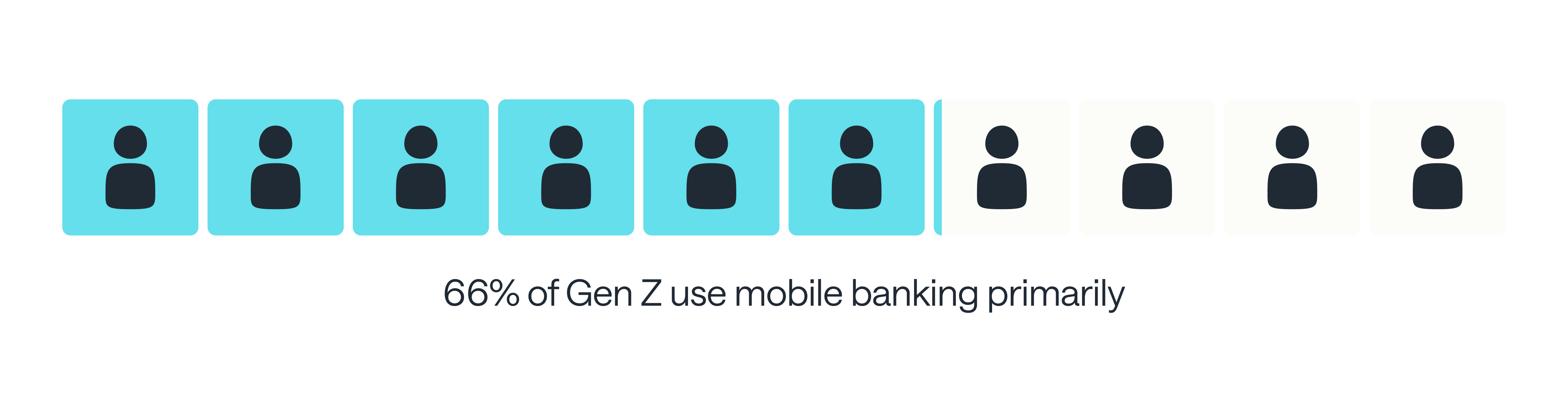

Gen Z and younger millennials didn’t learn to manage money standing in line at a bank. They learned it on their phones. For many, their first real banking experience was mobile. It was immediate, accessible, and always within reach.

Today, linking a bank account to manage money is a familiar behavior. Most U.S. adults under 30 already connect their bank accounts to track spending, move funds, and use services like digital wallets, investing platforms, and gaming apps. These experiences reinforce the idea that financial interactions should feel direct and transparent, with clear confirmation along the way.

Because these consumers already link their bank to spend, save, and invest, they are primed to do the same for payments across more traditional use cases. Research into how consumers choose and use payment methods shows that this is how these younger generations already behave, not just how they say they want things to work

For Gen Z and younger millennials, confidence at checkout starts with convenience. But convenience doesn’t just mean fast. It means intuitive, digital-first, and easy to understand in real time.

They want to know where their money is, what just happened to it, and whether it moved safely. That expectation carries over from how they already manage money day to day: checking balances, tracking activity, approving transactions directly from their phones.

Bank-connected payment experiences align with that preference. When transactions show up clearly and reflect what happened without delay, there's less mental math involved. Users don't have to think about statements, billing cycles, or what something will look like later. They can see it, understand it, and move on.

That clarity shapes how brands are judged in the moment. When a payment clearly shows what happened, it builds trust at checkout. When it doesn't, these younger generations pause, second-guess, or walk away.

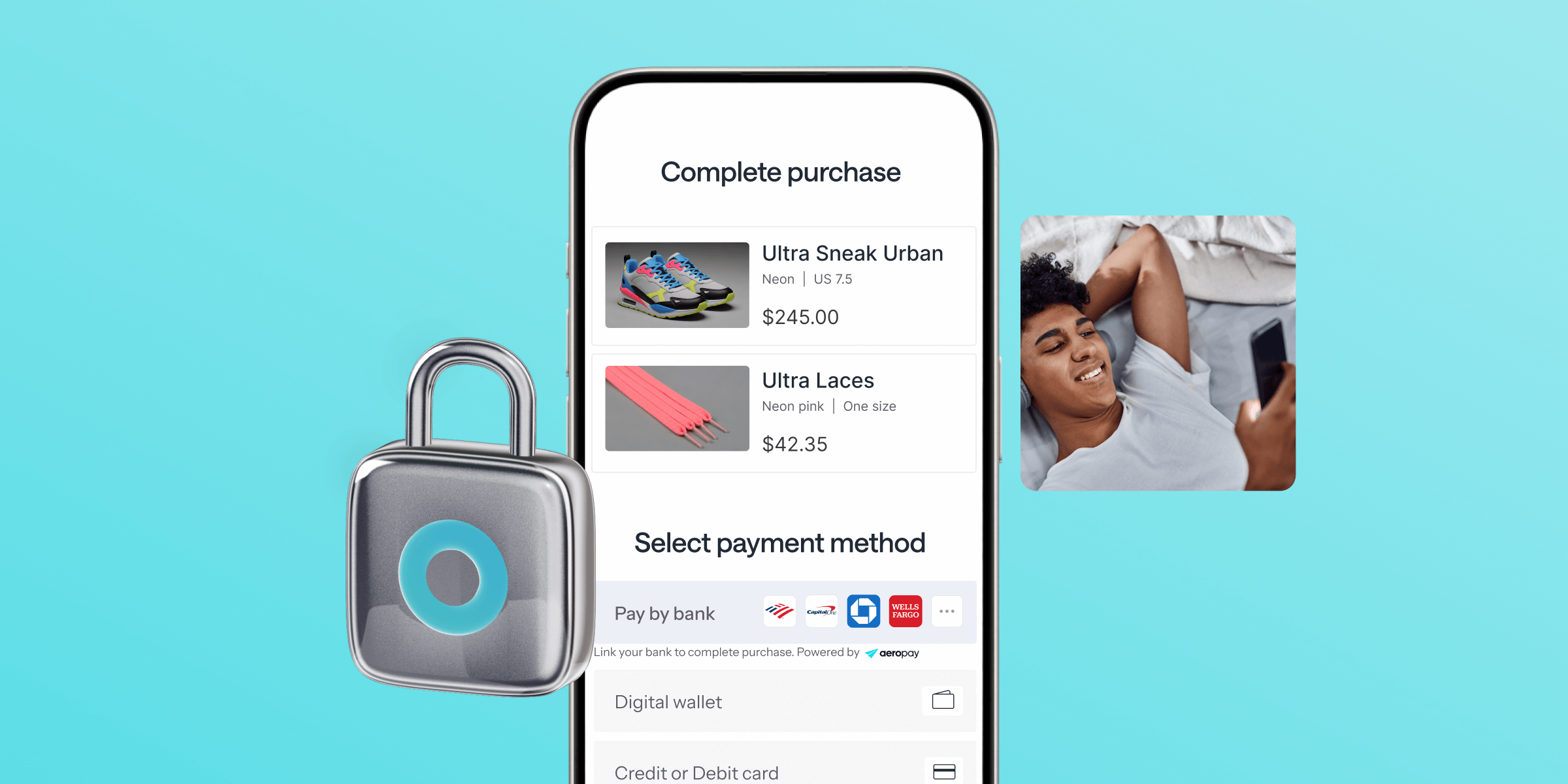

For Gen Z and younger millennials, proving who they are online usually means logging in, approving access, or confirming an action. Authentication isn’t friction—it’s familiar.

That's why authentication-based payment flows just work for people. When you approve a payment through a login or quick verification, it feels like how money is supposed to move. It's familiar. It makes sense. It's basically what these young people are already doing everywhere else.

Compare that to old-school ACH flows where you're hunting down routing numbers and manually typing in account digits. That experience feels like it's from another era. Few people are comfortable managing their money that way today. It’s clunky, it feels risky, and it’s disconnected from the instant, seamless experiences people now expect.

Manual card entry isn’t much better. Typing in long card numbers, expiration dates, and security codes adds friction at the worst possible moment. Sometimes you even have to stop and dig out your actual wallet, which completely breaks the flow. For people used to approving things with a tap or a quick Face ID, that interruption feels painfully slow.

The familiarity of authentication also shapes how secure a payment feels. When checkout mirrors the same steps you use to check your balance or authorize a transfer, it just signals legitimacy. That consistency really matters, especially when you're paying a brand for the first time or dropping more money than usual.

For brands, these expectations go beyond just usability. Checkout flows actually shape how modern, secure, and trustworthy your business feels. When payment interactions reflect the authentication behaviors people already know and trust, that confidence carries through to the transaction. And when they don’t, trust can start to erode before the purchase even goes through.

Modern tech has basically trained us to expect things to just work. Apps load instantly. Messages send without a second thought. Transfers happen and you get that little confirmation. So when something doesn’t work, can you really blame them for abandoning ship?

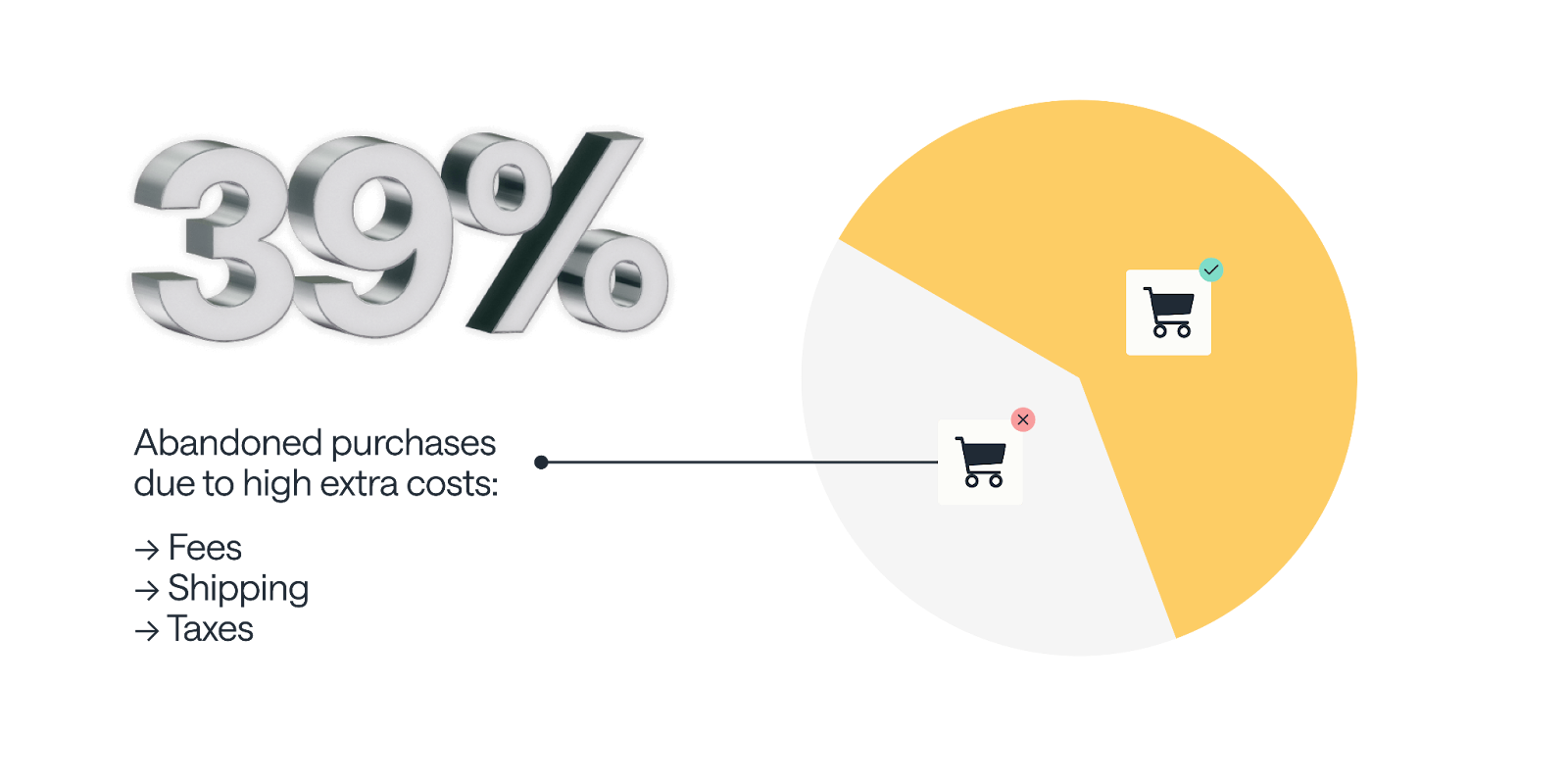

Younger generations seem to feel this more acutely. They didn’t grow up working around clunky systems. They grew up replacing them. The research backs this up, too. Studies on checkout usability continue to show that friction and payment hiccups are among the top reasons shoppers abandon a purchase, even when they fully intend to buy. When that final step breaks, most don’t stick around to troubleshoot. They just bail.

This same aversion to surprises shows up in how Gen Z and younger Millennials think about credit cards. Fees that pop up at checkout. Surcharges for using a certain method. Interest that quietly compounds in the background. For a generation that tends to be debt-aware and budget-conscious, those wild cards feel risky. A lot of them would rather avoid debt than chase reward points.

So predictability and control? They matter here. Payments that feel transparent and straightforward actually reduce stress in real time. And when it comes to payments, reducing stress is often what builds trust.

These behaviors have real consequences. When checkout gets clunky, younger consumers just... leave. That's not just a lost sale right now. It's potentially a customer who never comes back.

But when payments actually feel natural? When they work the way people already handle their money? Everything changes. More transactions go through. Customers feel better about the experience. And those good experiences start to stack up, turning one-time buyers into regulars.

Loyalty isn’t automatic for Gen Z and younger millennials. They’ll switch without much hesitation.

They grew up in the age of choice. Streaming replaced cable. Ride-share replaced taxis. Dating apps replaced blind dates. If something doesn’t work well, they’re used to having another option a tap away. Trying something new feels normal, not risky.

That mindset carries straight into financial services. Consumer research keeps showing that younger shoppers report lower brand attachment and a higher willingness to experiment than older generations. When experiences fall short—a clunky checkout, unexpected fees, a failed payment—they're more likely to explore alternatives than just put up with the friction.

The expectation isn’t loyalty by default. It’s loyalty that renews itself, every single time. Bad experiences carry real weight. A frustrating payment moment can reopen the question of whether this is a brand worth trusting next time. Once that question is open, competitors are a tap away.

Each interaction either reinforces trust or chips away at it. In an environment where switching takes minutes, experience is the only moat you've got.

Gen Z and younger millennials aren’t just being picky about checkout. They’re quietly resetting what “normal” feels like. They expect to see exactly what happened, get quick answers if something goes sideways, and avoid surprise charges or unclear timelines. That baseline carries over from how they already manage money in bank apps and P2P tools.

You can already see where this is heading in the infrastructure underneath it all. Bank-to-bank money movement operates at enormous scale through ACH, and usage keeps growing, including Same Day ACH. That steady volume isn’t flashy, but it matters. It shows that direct-from-bank payments are familiar territory for millions of people.

The shift isn't just technical. It's behavioral. Pay by bank already mirrors the financial tools younger consumers trust. For many, the appeal is immediate. Some brands are adding incentives like faster refunds or cashback to stand out at checkout, but the core advantage is built-in: when a payment method feels native to how someone already manages money, trust comes naturally.

If younger customers reward payment experiences that feel transparent and aligned with how they already move money, that’s a strong signal for merchants. What they normalize now tends to become the expectation every checkout has to meet later.

Gen Z and younger Millennials may be the clearest signal of where payments are heading, but they're not the only ones shaping expectations. The standards they normalize (clarity, speed, visible control) don't stay generational for long. They become the baseline everyone else has to meet.

The businesses paying attention now aren't simply adapting to a younger audience. They're aligning with a new baseline for checkout, one defined by transparency, familiarity, and experiences that feel consistent with how people already manage their money.