AI, instant payments, open finance, and pay by bank were some of the most talked about concepts in 2025. This was a year filled with challenges and innovative changes that ultimately moved payments closer to the optimal efficiency we expect across every other touchpoint in our modern age.

In the United States, bank payments have gone through a modern transformation. Instead of entering account and routing numbers, consumers can safely sync their bank in a click to pay (and get paid) for almost anything. This is due to the new standard providers like Aeropay have built to make online bank payments as easy and successful as cards.

In 2025, more US businesses than ever tapped into the unique value of pay by bank, powering smarter, safer, more affordable payment experiences at scale. Let’s take a look at the key changes driving the next generation of payments, and look ahead at the exciting innovations to come in 2026.

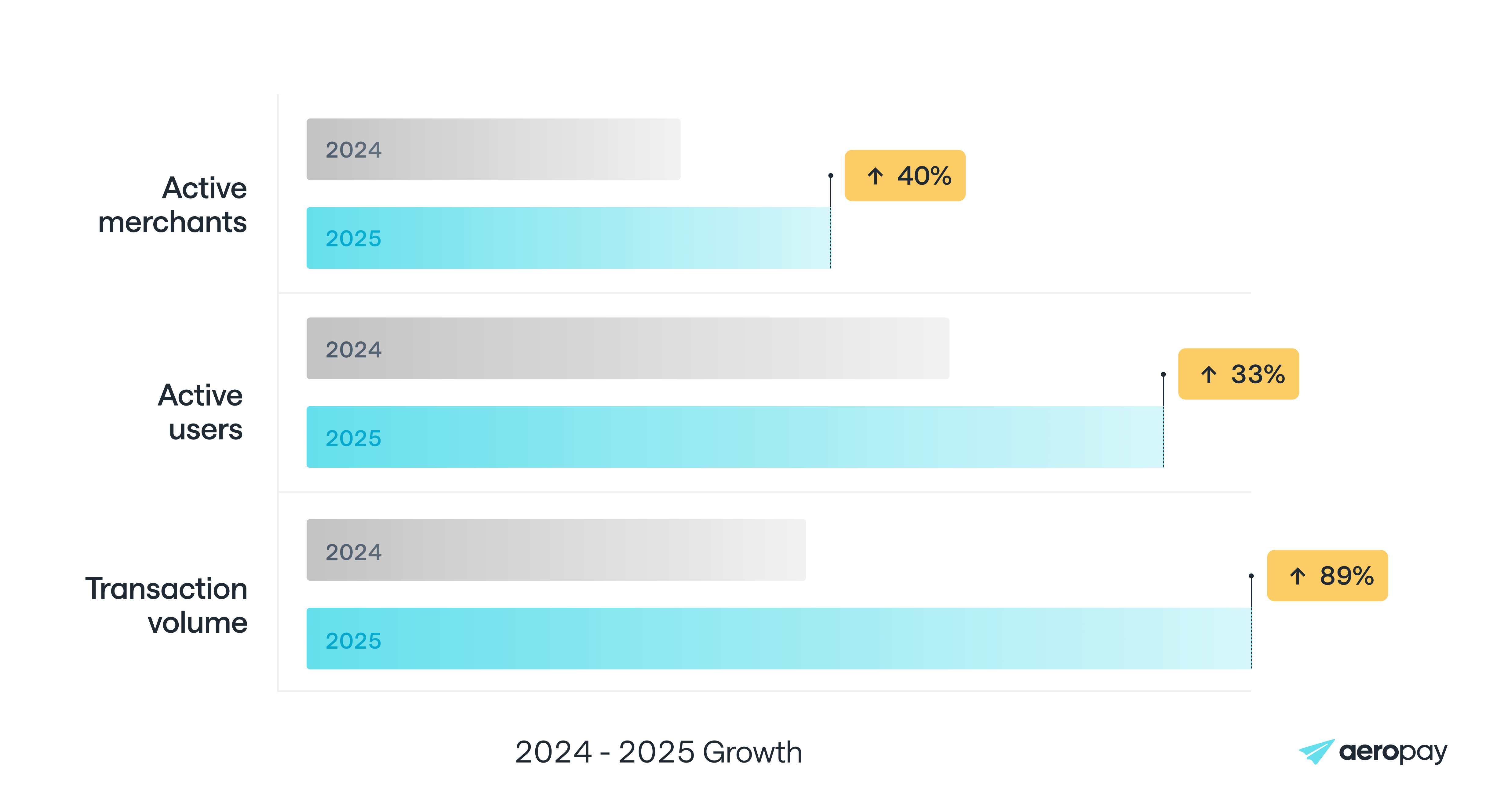

In 2025, Aeropay saw record growth across every core pay by bank metric. More businesses adopted pay by bank as a primary payment method, pushing active merchants up over 40% year over year.

More consumers followed, with active users growing by a third as pay by bank became a familiar, trusted way to move money.

Total transaction volume nearly doubled, driven by larger transaction sizes and more frequent usage across high-value use cases.

At the same time, instant payout volume increased 88%, reflecting growing demand from users to access their money instantly.

The same growth was present across the bank payment ecosystem. The RTP network nearly doubled value in 2024 to $246B across 343M transactions and then hit $481B in Q2 2025, a 195% jump in value vs Q1 as higher-value instant payments took off. Aeropay saw a similar 88% increase in RTP volume across businesses that enable instant payouts to their customers.

Same Day ACH continued to grow, with a 15% jump in Q3 2025.

58% of U.S. FIs that support instant payments now use both RTP and FedNow, not just one or the other. This signals maturity and redundancy. PYMNTS notes that “a multi-rail strategy increases resilience, providing backup and continuity that minimizes disruptions and strengthens operational integrity.”

From a global perspective, pay by bank is already a mainstream way to move money. In markets like India, Brazil, and across Europe, account-to-account payments have become one of the most popular payment methods, across use cases.

India’s UPI network now processes tens of billions of transactions per month, powering everything from peer-to-peer payments to large-scale commerce. Brazil’s Pix system surpassed cards in transaction volume just a few years after launch. In Europe, open banking-enabled payments have steadily expanded across e-commerce, bill pay, and subscriptions, supported by mature regulatory frameworks and widespread consumer familiarity.

There is a massive opportunity for businesses in the United States to leverage similar account-to-account. 2025 has shown this to be true, in a year where new advancements made it easier than ever to integrate pay by bank, convert consumers, reduce risk, and guarantee settlement.

For years, speed was the biggest tradeoff in bank payments. ACH was affordable and reliable, but slow. Cards were instant, but expensive and risk-prone.

That gap is now closing.

In 2025, businesses gained the ability to accept instant pay-ins directly from consumer bank accounts using real-time rails like RTP. Instead of waiting days to confirm settlement, merchants can now receive funds immediately — with confirmation at the moment of payment.

This shift fundamentally changes how bank payments compete with cards. Instant pay-ins allow merchants to offer a low-cost, high-trust option without sacrificing speed or user experience, unlocking new use cases across ecommerce, marketplaces, gaming, and high-value digital transactions.

The result: faster access to funds, better cash flow, and more flexibility in how businesses design their payment flows.

As the rails matured, pay by bank expanded well beyond its traditional strongholds.

In e-commerce, identity-powered checkout provider Skipify introduced pay by bank as a first-class payment option, helping merchants add a highly secure, affordable acceptance method alongside cards and wallets. By combining identity, authentication, and bank payments, e-commerce brands can reduce fraud while improving conversion — without passing higher costs onto consumers.

In gaming, pay by bank emerged as the fastest-growing payment method across several platforms. As transaction sizes increased and instant payouts became table stakes, operators turned to bank payments to move money in and out quickly, safely, and at scale.

Mobile platforms also opened new doors. In 2025, a U.S. appeals court ruled that Apple must allow iOS apps to link out to external payment options. Developers can now direct users to alternative checkout flows — including pay by bank — without Apple blocking or technically restricting those links.

While Apple may still be allowed to charge a “reasonable commission” on off-app purchases, the ruling materially changed the landscape for mobile payments. For the first time, pay by bank became a viable option for in-app purchases on iOS, expanding its reach into one of the largest digital commerce surfaces in the world.

Artificial intelligence was everywhere in 2025 — from personalized checkout experiences to real-time risk analysis and fraud prevention.

In payments, the most effective applications of AI are not fully automated systems operating in isolation, but models paired with human oversight. As fraud tactics become more sophisticated, especially with AI-enabled identity manipulation, payments providers are leaning on AI to analyze patterns, assess trust, and make smarter decisions at transaction speed. Read more about AI and fraud here.

Consumer sentiment reflects this balance. A Worldpay report found that while 44% of Americans say they are comfortable with AI-enabled shopping — rising to 59% among ages 18–34 — their biggest concerns remain identity theft, unauthorized purchases, and fraud. Trust and control continue to be the gating factors for adoption.

For pay by bank, AI is a growth enabler. It helps determine which rail to use, when to offer guaranteed settlement, and how to optimize for cost, speed, and risk — all without adding friction for the user.

Open banking was a constant point of discussion throughout the year.

Section 1033 of the CFPB’s open banking rules was finalized in late 2024, then partially blocked in 2025, leaving the industry in a state of regulatory limbo. Questions around liability and whether banks can charge for data access slowed formal progress, prompting some financial institutions to take matters into their own hands while courts and regulators debated next steps.

In practice, however, this uncertainty did little to slow pay by bank adoption.

Even without perfect regulatory clarity, demand for bank-powered payments kept climbing. Merchants want stable, secure access to financial data — not politics. Providers that already support OAuth-based bank connections, real-time data capabilities, and strong compliance infrastructure continued to pull ahead.

It’s a misconception that pay by bank is dependent on the fate of Rule 1033. Bank payments have entered the market as a flexible, affordable addition to merchant checkouts, not as a regulation-dependent mandate.

Data aggregators like Aerosync have already established direct OAuth connections with thousands of U.S. banks, enabling secure, frictionless authentication without outdated screen scraping. For institutions without OAuth support, alternative verification methods have emerged that avoid both screen scraping and microdeposits.

These innovations make pay by bank highly secure and user-friendly today — and position it to scale even faster in 2026.

As pay by bank enters its next phase, the conversation is shifting from adoption to optimization. Here are some of the biggest pay by bank trends to watch in 2026. Hear what Aeropay's experts predict for 2026 in this video.

The next wave of sophistication lies in orchestration. Instead of choosing a single rail, leading merchants will route transactions dynamically based on speed, cost, trust score, liquidity, and regulatory constraints. Instant pay-ins, guaranteed ACH, Same Day ACH, and instant payouts will coexist and be used intentionally.

The fastest in, fastest out, lowest cost, lowest risk combination will win. And the businesses that are set up to build that balance will pull ahead.

Card surcharging is getting hard to ignore. More merchants are adding explicit fees at checkout to offset card acceptance costs, and consumers are starting to notice how often that happens. What used to feel like an edge case now shows up in everyday purchases, from restaurants to services to digital transactions.

The math is what’s driving the frustration. Many consumers are paying an extra 3 to 5 percent to use a credit card in order to earn rewards that often amount to about 1 percent cash back. As awareness grows, that tradeoff is starting to feel less like a perk and more like a penalty. The surcharge may be compliant, but it still feels like a surprise fee, especially when it appears late in the checkout flow.

This creates friction for businesses. Card networks allow surcharging, but only under strict and uneven rules, and the customer experience is difficult to get right. Even when fees are disclosed correctly, they introduce tension at the moment of payment, which is rarely where businesses want to negotiate price.

By eliminating interchange costs, pay by bank helps merchants avoid having to pass fees onto customers altogether. As consumers become more cost-aware in 2026, payment methods that reduce the need for surcharges will stand out not just for savings, but for delivering a more transparent and trusted checkout experience.

Recurring payments represent one of the largest untapped opportunities for pay by bank.

This is because bank accounts are highly stable. The average checking account in the U.S. is 18 years old — and even among 18- to 24-year-olds, the average account age is seven years. Credit cards, by contrast, are frequently reissued due to expiration, loss, or fraud.

That instability creates friction for consumers and unnecessary failure points for merchants.

While billing has historically been a heavy adopter of traditional ACH payments, pay by bank can provide these businesses with greater transparency, higher approval rates, lower risk, and considerably higher revenue.

As payments move faster, compliance is being forced to change with them.

One of the most important shifts coming in 2026 is a new NACHA rule that requires everyone involved in ACH payments to conduct risk-based fraud monitoring. Historically, that responsibility sat mostly with banks. Third parties followed their lead, and accountability wasn’t always evenly distributed.

That model is ending. Going forward, every participant in the payment flow is expected to take responsibility for monitoring risk. The intent is straightforward. Catch fraud earlier, reduce surprises after settlement, and increase confidence as bank payments continue to grow and transaction windows get shorter.

Read the Q&A with Geoffrey Scott for the top 2026 compliance trends, from data-sharing rules and AI oversight to the future of embedded payments.

Stablecoins are gaining momentum, especially for global movement of money. But even as tokenized dollars grow, they still rely on bank-linked on- and off-ramps to acquire users, convert value, and settle into fiat.

For merchants, this reinforces the role of pay by bank as the trusted bridge between digital-dollar rails and the traditional banking system. As stablecoins move deeper into remittances, ecommerce, gaming, and marketplaces, demand will increase for compliant KYC/AML processes, smooth account funding, and instant cash-in and cash-out experiences.

Rather than cannibalizing pay by bank, stablecoin adoption is likely to amplify it — driving more account-linked flows and more demand for instant, compliant infrastructure.

In 2025, we introduced a refreshing new look for the Aeropay brand to reflect our next chapter as America’s pay by bank network. This new chapter will cover new use cases, new partners, new customers, new products, and a far wider network of users.

In 2026, expect to see Aeropay pushing the envelope as the premier option for modern bank payments in the United States.

We look forward to helping more businesses lower costs and increase revenue with the simplicity and success of pay by bank.

Happy New Year!