Bank account linking: What it really takes to scale pay by bank

Payments

May 12, 2026

|

Nate Sousa

Nate writes content for Aeropay. His mission is to make pay by bank clearer and easier to understand for everyone.

Bank payments make a lot of sense on paper. Lower costs, no card network taking a cut, money moving directly from a customer's account to yours. For high-volume businesses, the math is hard to ignore.

But there's a gap between adding bank payments and actually making them work. A payment method that sits in your checkout but doesn't get used doesn't save you anything. And one that gets initiated but fails too often starts costing you more than you saved pretty quickly.

The businesses that are winning with bank payments aren't just the ones that flipped the switch. They're the ones that set it up properly. They get customers through the linking flow, keep payments moving, and make the second transaction easier than the first.

The setup matters more than most businesses expect. Here's what actually makes them work.

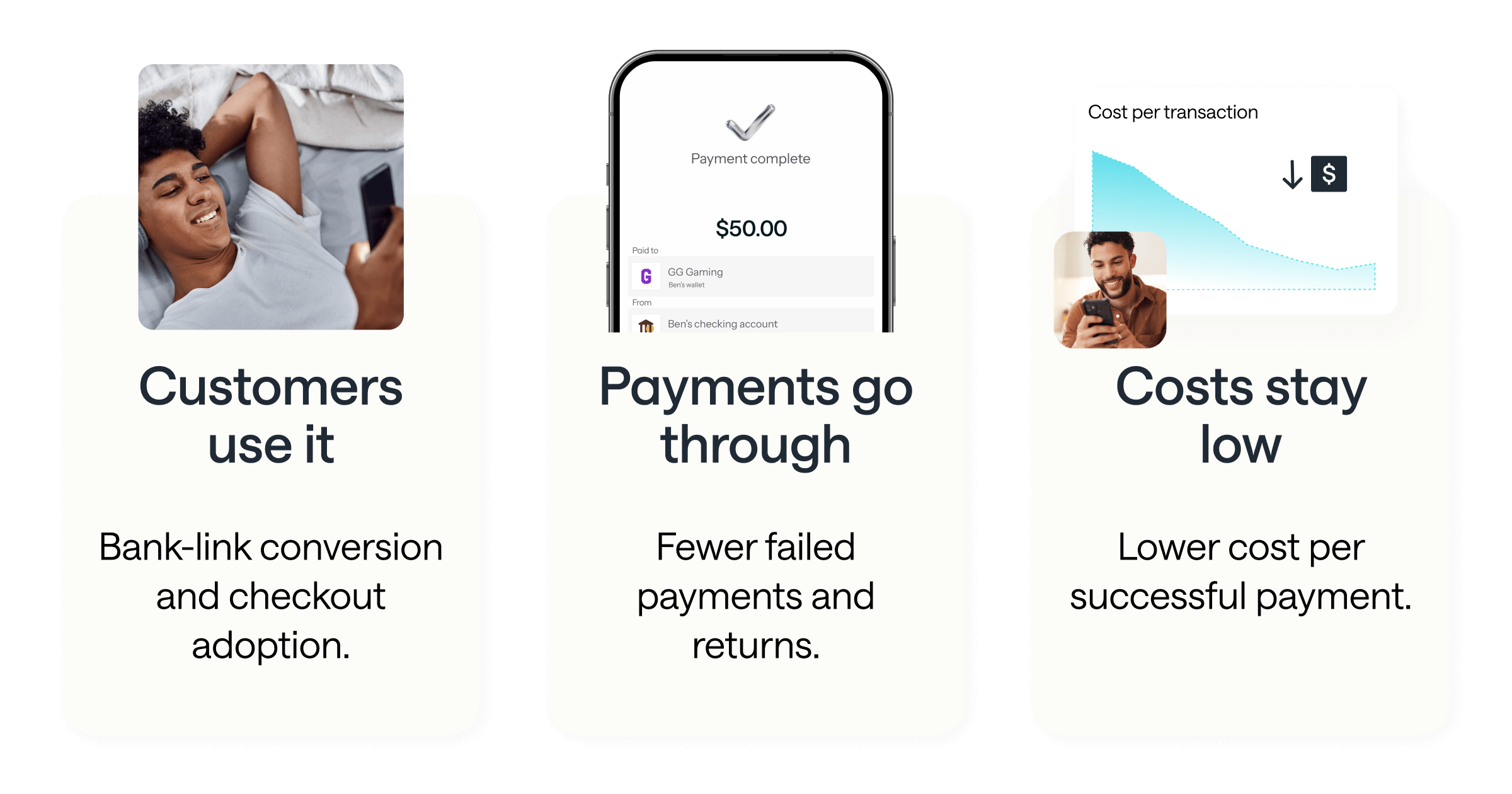

Think of bank payments like a two-part handshake. The customer has to show up and reach out. That's the adoption piece. And the other hand has to meet them. That's the payment actually going through. If either side drops, the whole thing falls apart.

It sounds obvious, but it's easy to miss when you're evaluating bank payments mostly on price. A 0.5% transaction fee looks great on a slide. It looks a lot less great when a meaningful chunk of your customers are dropping off before they finish linking their account, or when enough payments are failing and returning that you're spending time and money cleaning up the back end.

So before anything else, it helps to be clear about what "working" actually means here. Customers need to find the experience easy enough to actually complete. And once they do, payments need to go through reliably enough that the math still works. Those are two different problems, and solving one doesn't automatically solve the other.

A bank payment that doesn't go through isn't a cheaper payment. It's just a failed one.

Before a customer can pay by bank, they have to connect their account. That step is called bank linking and is easy to overlook when you're thinking about payment strategy.

If the linking flow is confusing, slow, or asks for more than someone is willing to give at that moment, they leave. And once they leave, the payment never happens, and not because they didn't want to pay. Because the path felt like too much work. Payment friction is one of the leading causes of checkout drop-off, and bank linking adds an extra step that most payment methods don't require. That step has to earn its keep.

Strong bank linking doesn't just improve adoption either. When a customer connects a verified, active account, you have better signal about the payment before it's even initiated. That’s a much stronger starting point than a manually entered account number you can't validate until something goes wrong.

Not all bank linking is built the same, and that's something most businesses only figure out after they've already committed to a solution.

Manual account entry (where a customer types in their routing and account numbers) is slow, error-prone, and creates no real foundation for future payments. One typo and you're chasing a return. Generic account-linking tools can do better, but many are built with payments as an afterthought. They connect accounts well enough, but "connected" and "ready to pay" aren't always the same thing.

The gaps tend to show up in a few places: verification steps that add unnecessary friction, API charges that stack up fast (often for data that should be cheap to access), customers who have to re-link accounts they've already connected elsewhere. None of these are dramatic on their own. But together they make bank payments harder to scale and less cost-effective than advertised.

Most bank linking infrastructure was built for account access, not payment outcomes. That has real consequences for conversion, return rates, and what it actually costs to process a successful payment.

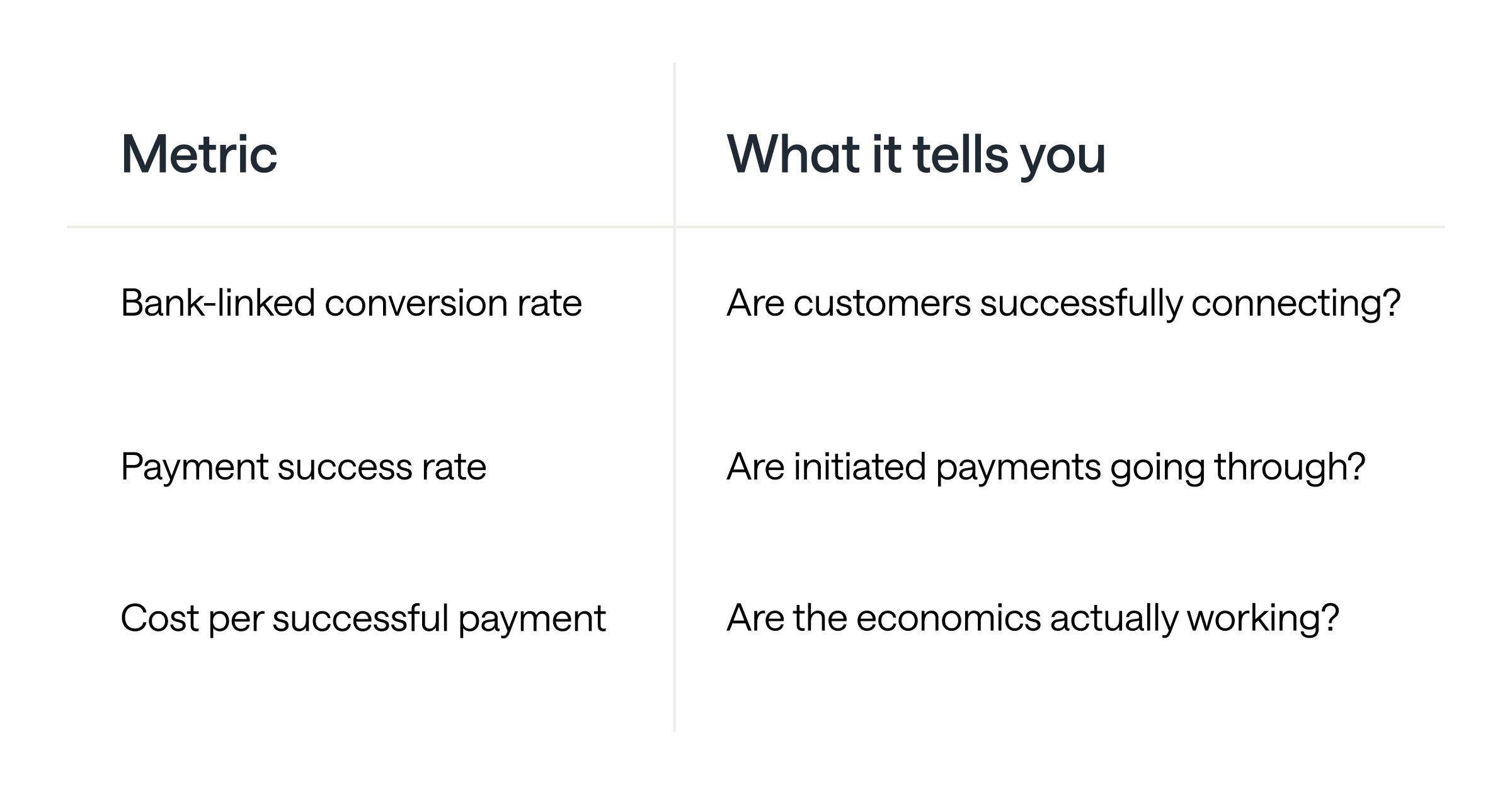

If you're evaluating whether bank payments are actually working (not just available, but performing) there are three metrics that tell most of the story.

Bank-link conversion rate: Are customers successfully getting through the linking flow? This is the number that reveals whether your bank payment option is actually accessible or just technically present.

Payment success rate. Of the payments that get initiated, how many actually go through? Failed payments don't just cost you the transaction, they create cleanup work on the back end and erode customer trust in the method.

Cost per successful payment. This is the one that tends to surprise people. A low transaction fee can look very different once you factor in failed payments, returns, and verification costs. The fee is what you pay. The cost per successful payment is what bank payments actually cost you.

Taken together, these three numbers give you a much more complete picture than transaction fees alone. They're also the right lens for evaluating any bank linking provider, because the difference between a good one and a mediocre one shows up here first.

The first time a customer links their bank account is almost always the hardest. There's a new flow to navigate, a level of trust being extended, a moment of "is this legit?" For a lot of customers, that first experience colors every transaction after it.

Which is why what happens next matters so much. If a returning customer has to re-link their account, re-verify their identity, or start from scratch in any meaningful way, you've lost the ground you already gained. The friction that made sense the first time becomes frustrating the second. And unnecessary the third.

Better yet, in networks where customers are already onboarded and verified across multiple businesses, they may not have to start from zero at all. They show up recognized, and the payment just works.

Aeropay's network already recognizes a significant portion of returning users across merchants. For some customers, that means skipping the hard part entirely, even on their first transaction with youThat's the version of pay by bank that actually sticks.

In the beginning, we used the top three aggregators for bank connectivity. Aeropay didn't come to bank linking from the outside. We scaled our own pay by bank product and ran into the same walls everyone else does: conversion dropping off in the linking flow, return rates that ate into the economics, repeat customers facing friction they'd already earned their way past.

The existing options weren't built for what we needed. They connected accounts, but they didn't optimize for payment outcomes. So we built Aerosync to do that specifically. It’s bank linking designed from the ground up around conversion, payment success, and repeat usage.

When we made the switch, the results were hard to argue with:

The returns improved. But so did everything upstream, like conversion, repeat usage, the whole flow. That's what building for payment outcomes actually looks like.

The businesses that win with bank payments won't be the ones that found the cheapest transaction fee. They'll be the ones that solved adoption, reliability, and repeat usage — and built infrastructure around all three, not just one.

A low fee doesn’t solve any of that. It gets you in the door but it doesn't get customers through the linking flow, keep payments from failing, or make the second transaction easier than the first. Those things require infrastructure that's built specifically for payment outcomes.

Bank linking is where the difference gets made. It's the step that determines whether a customer completes the flow or doesn't, whether the payment succeeds or returns, whether the economics hold or quietly fall apart.

That's what we built Aerosync to be. Not just another way to connect an account, but the part of the stack that actually makes pay by bank work.