Pay by bank is the most cost-effective, secure, and compliant payment option.

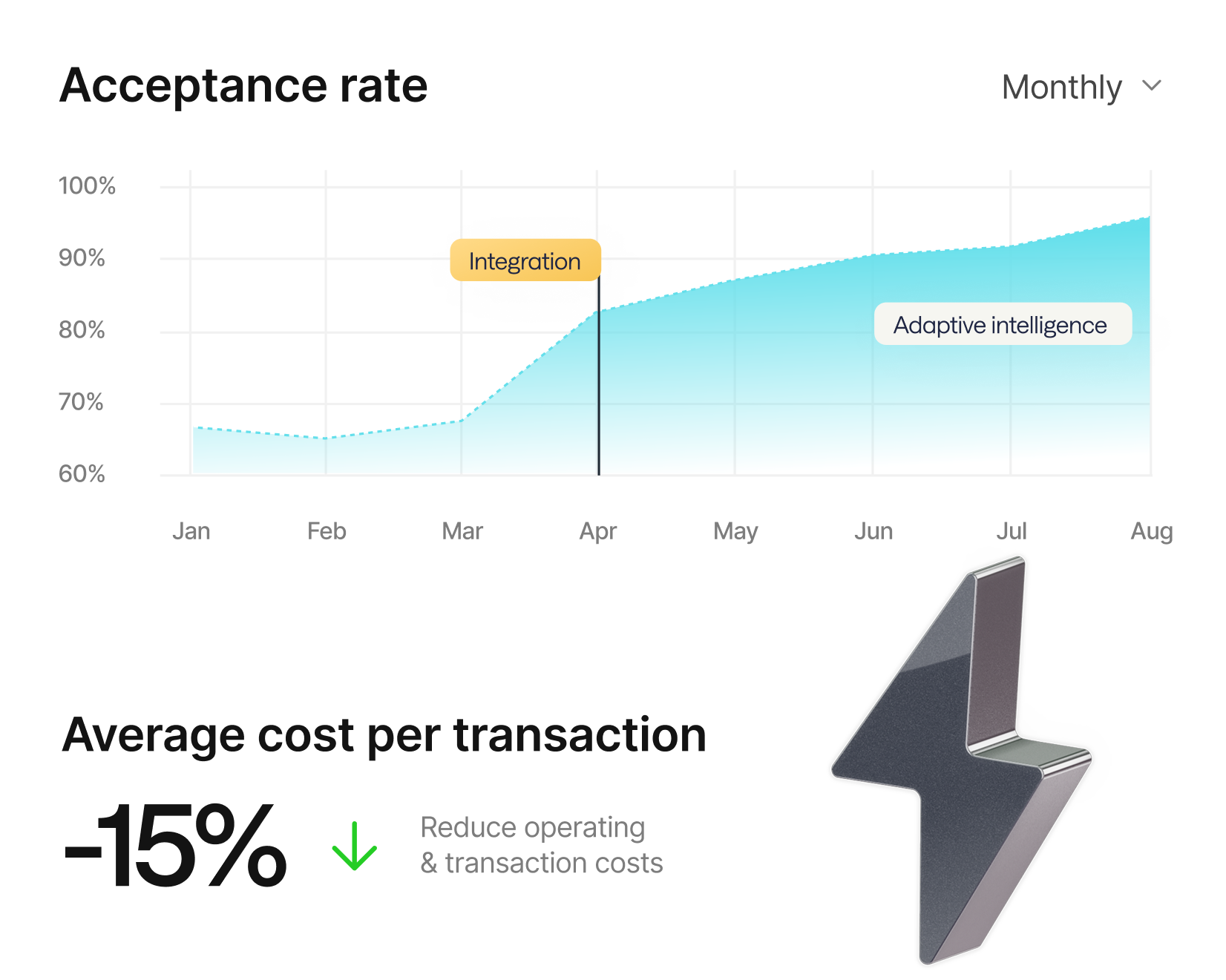

Same-Day ACH is up to 50% less expensive than card rails. Protect your margins and reinvest savings back into growth.

Built-in safeguards and transparent reporting help specialized retailers meet strict regulatory requirements without slowing down payments.

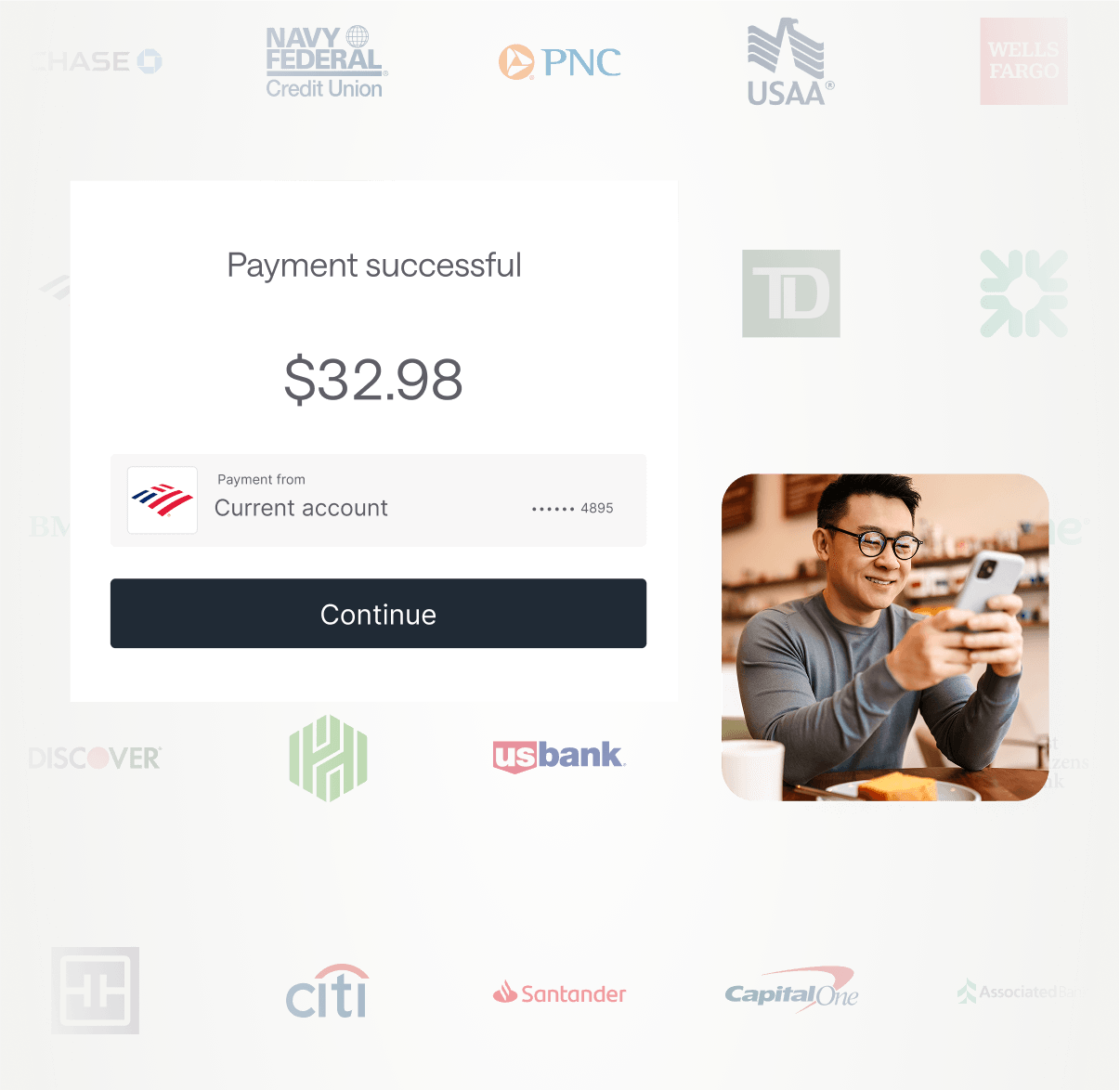

Higher approval rates and guaranteed ACH coverage mean fewer failed payments, higher revenue, and more reliable cash flow.

One integration handles compliance, settlement, and reconciliation—reducing back-office work so your team can focus on customers.

Easily capture tips in the same seamless flow as payments. Flexible tipping options help increase staff satisfaction while keeping reporting clean and compliant.

Automate repeat purchases with secure, scheduled payments. Reduce failed transactions and improve customer retention without adding staff workload.

See every transaction as it happens. Real-time visibility improves cash flow management and reduces reconciliation headaches at the end of the day.

Control multiple storefronts from a single dashboard. Send location-specific links, monitor performance, and standardize operations.

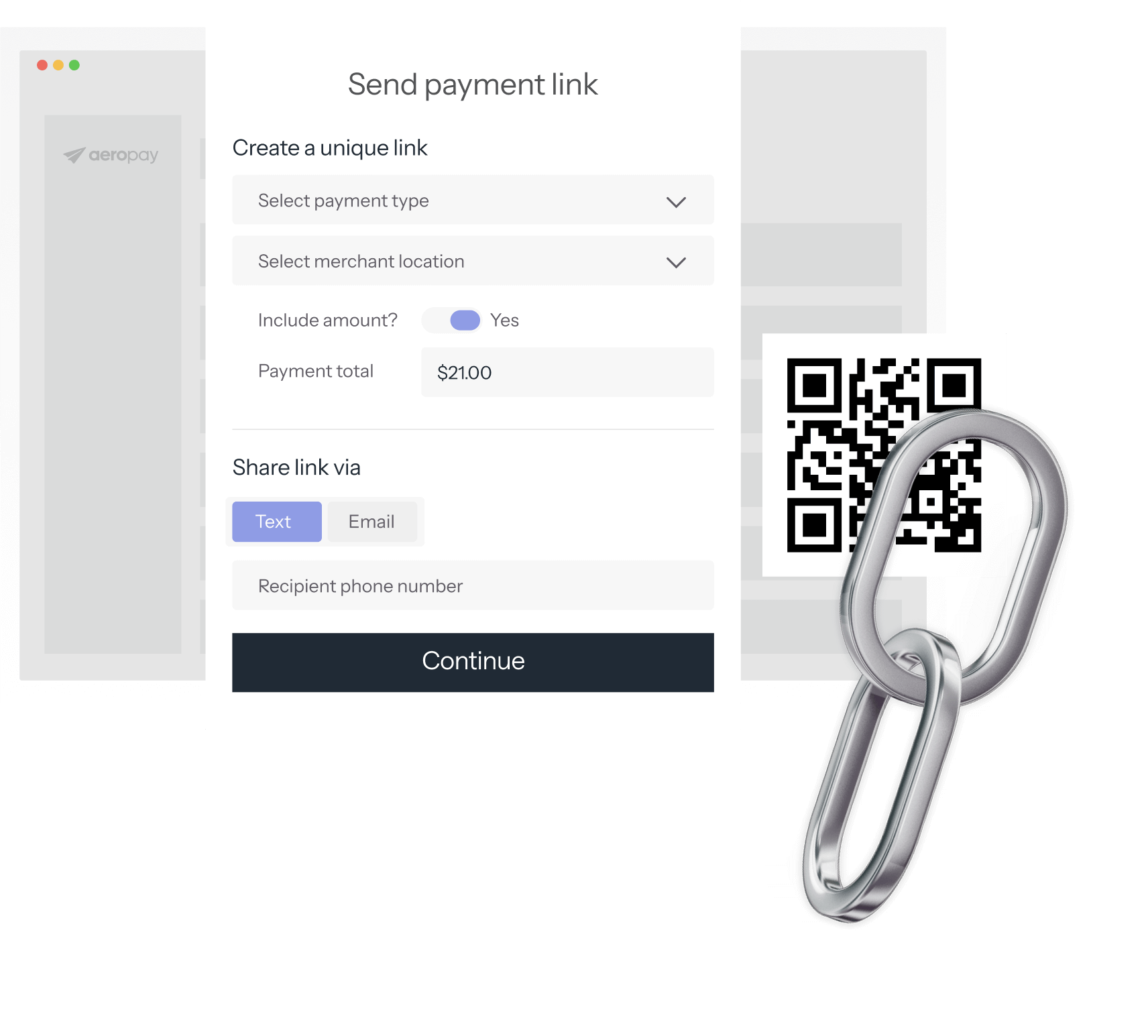

Modernize the checkout experience for however your customers shop.

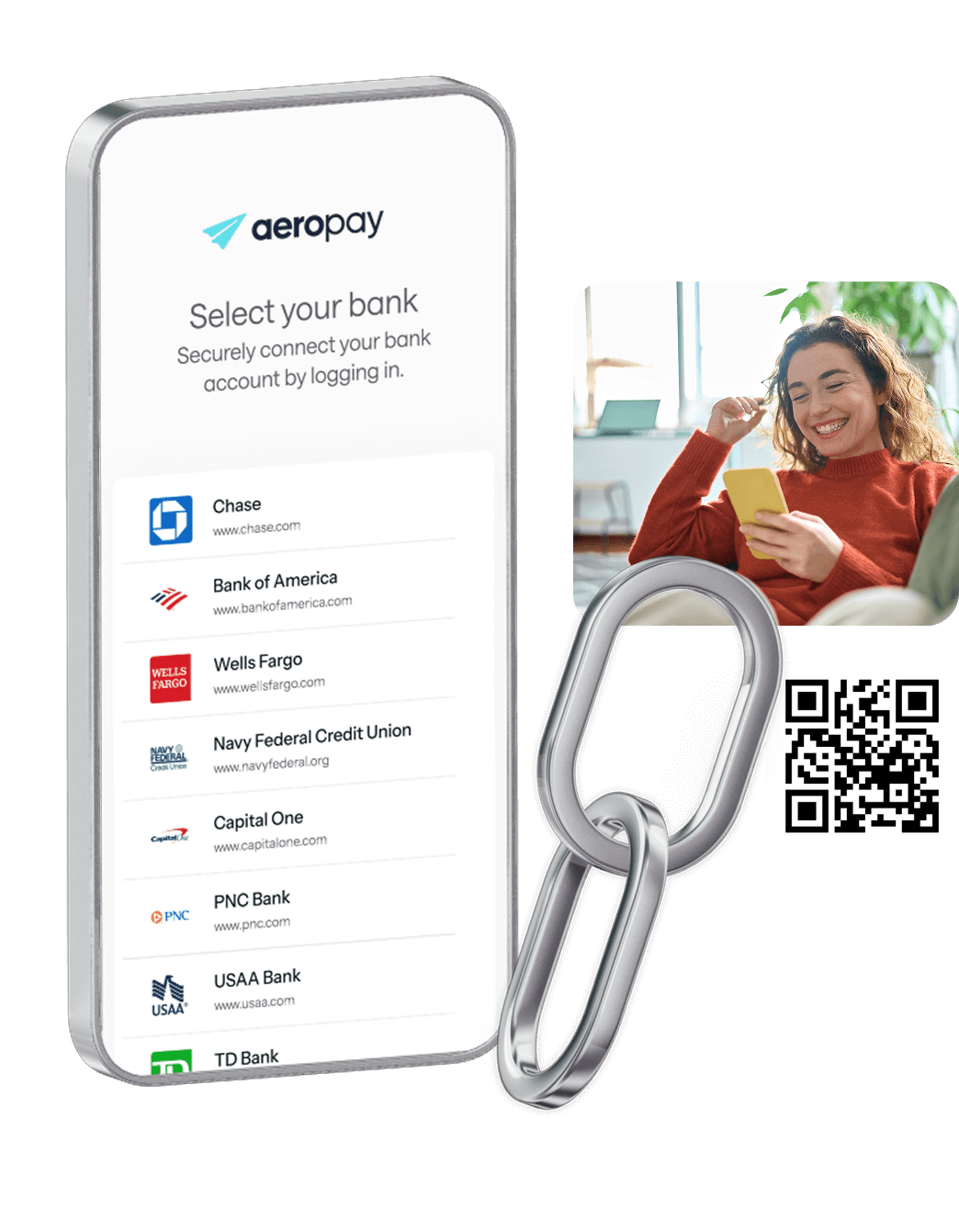

Customers simply scan a QR code at checkout to pay with their bank account. Or, generate a payment link and share directly to your customers via email or text message.

Add integrated online payments for delivery orders. It’s the same familiar sign up and payment flow — with capabilities for routing integration, driver tipping, and more.

With Aeropay’s pre-payments, customers can submit a payment online that’s finalized once they receive their order. Enable authorized payments in advance to easily adjust or cancel orders.

Boost online orders and drive foot traffic with integrated payment solutions that enhance customer satisfaction and unify the shopping experience across channels.

Cashless ATMs and similar workarounds process regulated retail purchases as “miscellaneous transactions,” creating compliance risks and inflating fees. Regulators are increasingly scrutinizing these models. Aeropay, by contrast, offers a transparent, compliant pay by bank solution built specifically for regulated payments, giving both operators and regulators confidence in the process.

Wellness businesses, gyms, and healthcare providers often rely on recurring billing for memberships or care plans. Aeropay’s durable bank connections allow for automatic billing cycles without the risk of expiring or declined cards. Customers benefit from uninterrupted service, while businesses enjoy more predictable revenue.

Industries like healthcare and wellness have historically relied on cash, which creates security risks, theft exposure, and costly cash handling processes. Aeropay reduces these risks by digitizing payments, lowering the need for physical cash while improving audit trails and compliance reporting.

Aeropay enables specialized retailers to accept digital payments directly from customer bank accounts. This eliminates the need for cash-heavy operations, reduces risk for merchants, and provides customers with a modern, cashless payment option that feels as seamless as paying with a card or wallet.

Yes. Customers link their bank account once through a branded checkout flow and can pay in seconds, without needing to download a separate app. This improves adoption across demographics that may not want to install new payment apps, especially in industries like healthcare and wellness.

Card networks restrict regulated transactions, forcing many retailers to rely on cash or workarounds that create compliance risk. Pay by bank solves this by moving money directly between banks, outside the card networks. Aeropay partners with licensed financial institutions and complies with BSA/AML requirements, ensuring regulated payments are secure, transparent, and compliant.

Aeropay is registered as a money transmitter where required and complies with NACHA operating rules and BSA/AML standards. For CBD companies, Aeropay only partners with licensed financial institutions, ensuring transactions remain fully transparent and compliant with state and federal guidelines. For healthcare, Aeropay operates within HIPAA privacy requirements by design.

Healthcare providers can use Aeropay to accept bill payments, recurring care subscriptions, and telehealth visits directly from patient bank accounts. Unlike cards, which may create PCI and HIPAA compliance burdens, Aeropay processes payments securely without storing sensitive credentials. Instant refunds and recurring billing also improve patient experience and reduce administrative overhead.