Are Americans ‘Credit Healthy’? New Reports Signal Change

April 17, 2024

|

Rachel Ludwig

Collectively, Americans owe $1.13 trillion on their credit cards, a new record.

But many insist this debt isn’t concerning—yet.

While consumer debt has risen, delinquency on credit card payments hasn’t. It appeared Americans were simply paying with plastic, then paying off the amount owed each month.

Now, the tide may be turning.

The latest installment of VantageScore’s Credit Gauge shows delinquencies climbing across all tiers of credit — and for a range of credit products, including mortgages, credit cards, personal loans and auto loans.

Using recent data, news, and developments, this post examines U.S. consumer credit health to answer the question: Are Americans “credit healthy”?

Learn about financial inclusion in the United States.

In simplified terms, being “credit healthy” describes an ability to spend within one’s means.

This includes avoiding an unreasonable ratio between how much you’re spending and how much your credit cards authorize you to spend.

It also means avoiding late or delinquent payments.

Credit health is often tied to credit scores, but something called “credit utilization ratio” also signals whether an individual is credit healthy.

Credit utilization ratio = Sum of credit card balances / sum of credit lines

For example, if you have just one credit card with a $10,000 credit line and a current balance of $5,000. To find your credit utilization ratio, divide 5,000 by 10,000—which results in 0.50, or 50%.

It’s ideal to stay below a 30% credit utilization ratio to signal healthy credit.

The United States government holds the world's largest national debt in terms of dollar amount.

Total household debt in the U.S. is $17.3 trillion—a new high that’s fueled by a 16.6% increase in credit card spending between Q3 2022 and Q3 2023.

Debt (particularly credit card debt) isn’t common everywhere in the world. In fact, America's reliance on credit scores often means a jarring and complicated journey for immigrants who are new to the concept of paying for commodities with microloans.

But in a country where paying off debt is the key to building credit—and good credit is the key to accessing funds for a home, a car, and other life-enhancing assets—we’ve embraced paying with borrowed money.

However, there are “good” and “bad” sources of debt, and it’s increasingly common for Americans to lean into the latter.

Good debt is often considered an investment that will grow in value or generate long-term income. Taking on good debts can lead to improved financial outcomes if managed responsibly.

Examples include:

Bad debt is typically used to purchase depreciating assets or consumption goods that do not increase in value. Such debts can strain financial resources without providing any return.

Examples include:

In short, the average American is likely to take on some debt, but there are certain types that should be avoided, particularly when it comes to spending with credit cards.

While Americans have been managing credit card payments reasonably well even though spending is increasing, recent trends indicate a concerning shift.

VantageScore’s February Credit Gauge found early-stage credit card delinquencies are rising, exceeding 1.0% for the first time in four years.

At the same time, the VantageScore Prime credit tier contracted by 1.1% year over year with the largest moves “up” into VantageScore Superprime (781-850) or “out” into VantageScore Subprime (300-600).

Susan Fahry, Executive Vice President and Chief Digital Officer at VantageScore explains the latest report:

“The tale of two consumers is becoming more pronounced…VantageScore Superprime consumers are still spending and borrowing while VantageScore Subprime consumers are finding it increasingly difficult to stay current on credit payments.”

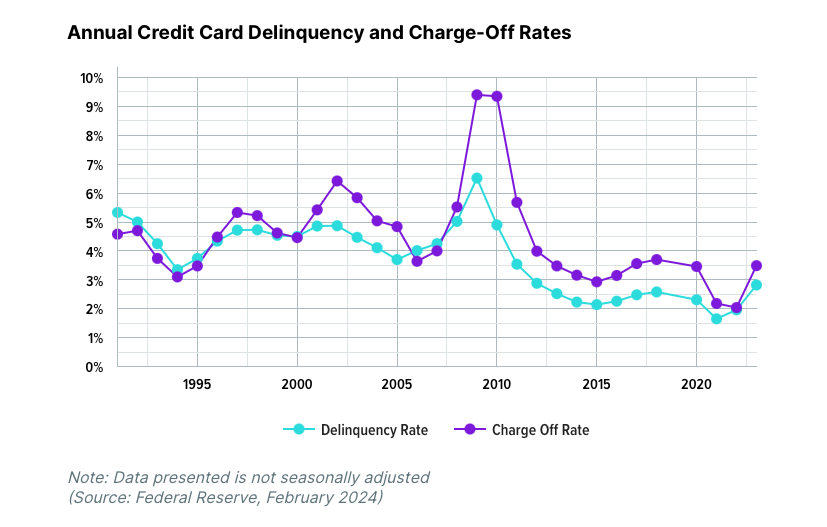

We see the bigger picture playing out in the Federal Reserve’s data on credit card delinquency rates which are climbing closer to levels from the 2008 financial crisis. The concern is mounting, but consumers are still swiping cards and spending.

As a leading digital payment provider, Aeropay offers a better option over credit cards via pay by bank for in-store and e-commerce business transactions nationwide.

Businesses using Aeropay experience:

The simplicity, security, and efficiency of Aeropay make it an easy choice for your customers—and your business.

Schedule a 15-minute demo to see our full payment solution and make bank-to-bank transfers work for your business.