Why Account-to-Account (A2A) Payments are a Viable Credit Card Alternative

February 5, 2024

|

Sam Ratcliffe

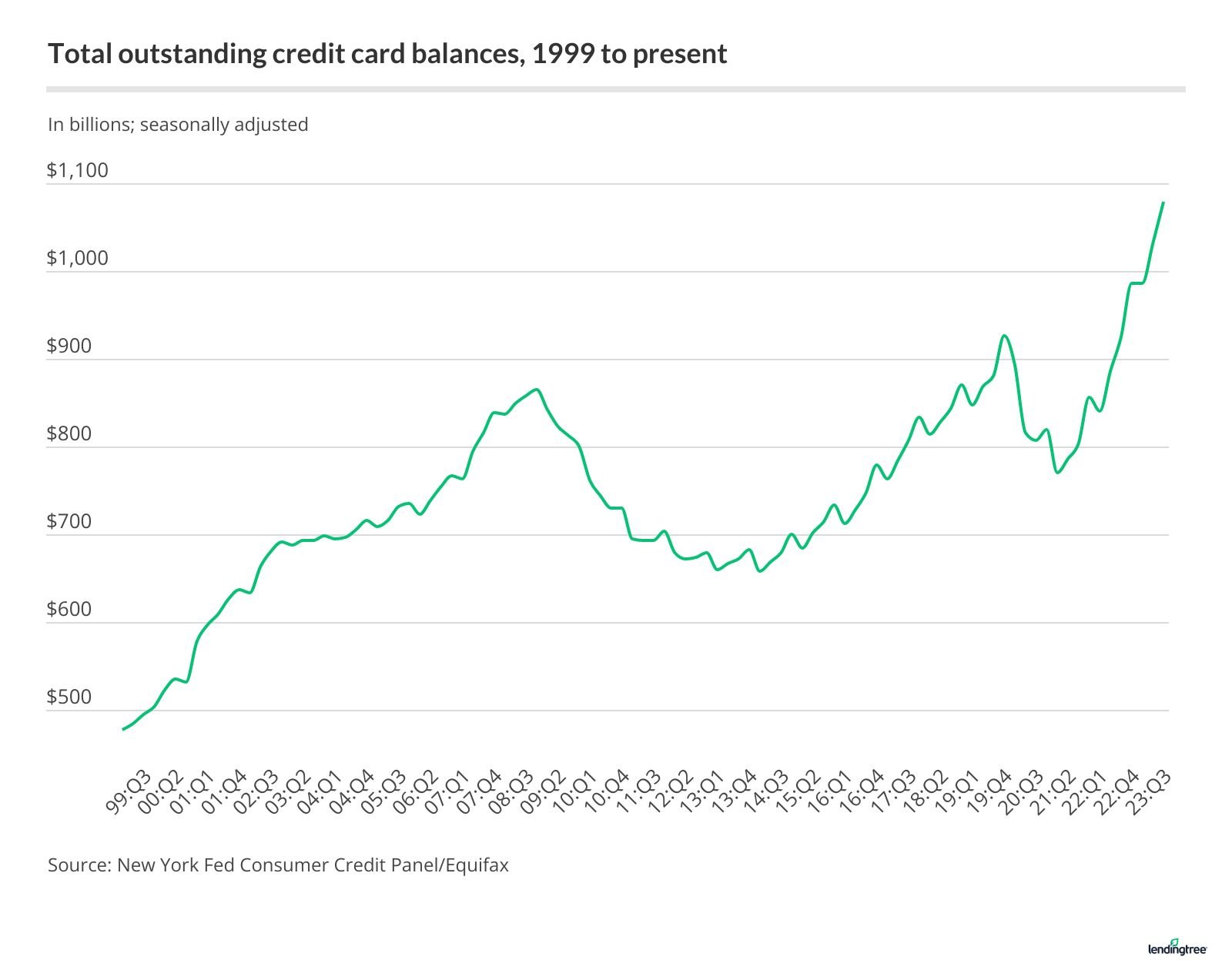

Americans are in record credit card debt of $1.079 trillion, according to recent data from the Federal Reserve Bank of New York.

This is largely due to a combination of economic factors and increased marketing tactics from credit card companies like Visa and Mastercard, as well as consumer credit reporting companies like Experian and even local credit unions and credit bureaus.

This is the highest level of consumer debt in history, but it also marks an opportune time for shoppers to choose a new, more trustworthy way to pay. Merchants can satisfy growing unrest toward high-risk payments by offering seamless non-credit options like account-to-account payments (also known as “pay by bank”).

While credit cards are helpful in many instances, they are easily misused. This leads to high interest rates, late payments, and revolving debt that’s only good for lenders. This hard-to-break cycle is mentally taxing, and 48% of Americans with revolving credit card debt say they are stressed about it.

In reality, credit card debt doesn't have to keep rising. Many of the reasons consumers choose to pay by credit can be replaced via A2A transactions.

This post explores why consumers depend on credit and how account-to-account payments are a reliable alternative.

The biggest reason people pay with credit cards isn’t actually to defer payment, build a better credit score, or get out of bad credit—it’s to earn rewards.

A survey by GOBankingRates found nearly 1 in 4 consumers say credit card rewards and perks are the primary purpose for using a credit card.

Conversely, only 2.48% use them to defer payment, meaning credit cards serve as high-risk “rewards cards” for many consumers.

Rewards are easily tied to A2A transactions, too. In fact, incentives will be why many consumers try the payment method. PYMNTS found that 41% of consumers who have not used A2A transfers in the last 90 days are open to trying them if offered incentive programs. Merchants can even send cash back rewards using options like Aeropay’s Real-Time Payment (RTP) network.

This is a sizable differentiator between A2A and the most common credit alternative, debit cards—which typically have no reward options.

💡Learn more about incentivizing A2A payments.

Takeaway: A large demographic of consumers use plastic just for the perks, but they can avoid the risk and added cost of credit cards by simply paying via A2A.

52% of consumers believe convenience influences at least half of their decisions—including their payment method. At the same time, 60% of consumers transacting with A2A payments say convenience is why they use the method.

In order to break the cycle of credit card spending, a payment alternative must be enticing and convenient.

Because A2A payments link consumer and seller bank accounts and immediately withdraw from their checking account, they can be done in a single click after the initial setup. This convenient way for customers to pay will help drive loyalty. In fact, Aeropay data shows a 70% increase in online customers returning when paying by bank.

Takeaway: Convenience is a deciding factor for most shoppers, and A2A’s simplicity, practicality, and user-friendliness will sway customers to begin and continue using the method over cards.

When compared with credit cards, A2A offers faster settlements, better security, and lower costs from fees.

For most credit card or debit card companies, it can take 3-7 days. With Aeropay, settlement time is the same day or next day.

A2A options like Aeropay enable multi-factor authentication (MFA) to secure accounts and have bank-level encryption, fraud prevention, and risk reduction measures built into every layer.

With A2A payments, there are no customer-facing fees and typically much lower transaction fees than credit cards.

Average credit card processing fees are 1.5% to 3.5% of each transaction. However, this does not include fees the business pays merchant services providers for payment gateways, equipment, and monthly account charges. In all, it’s expensive to accept a credit payment.

On the other hand, A2A payments are considerably more affordable for merchants and save them up to 70% on transaction costs compared to card transactions. They’re worth adding as a payment option, particularly as more customers apply pressure for adoption.

Takeaway: A2A transactions are settled faster, are more secure, and are far less expensive than credit cards, making them a win-win for consumers and merchants.

Traditional credit cards should be used to build good credit or emergencies. They were never originally intended for daily purchases that build an endless repayment cycle.

With the addition of new credit-focused payment options like “Buy now, Pay later” (BNPL), there will be more risk of consumer debt than ever.

One easy way to counteract this is with an exciting, easy-to-use payment option like Pay by Bank. Shoppers can still earn rewards (if incentivized) without annual fees, term loans, credit checks, credit limits, credit history, interest rates, or eligibility requirements.

Cardholders need new payment options to maximize financial inclusion. A2A is a perfect fit.

As a leading digital payment provider, Aeropay offers reliable instant payments for in-store and e-commerce business transactions nationwide.

Businesses using Aeropay experience:

The simplicity, security, and efficiency of Aeropay make it an easy choice for your customers—and your business.

Schedule a 15-minute demo to see our full payment solution and make bank-to-bank transfers work for your business.