By clicking Accept, you agree to the storing of cookies on your device to enhance site navigation, analyze site usage, and assist in our marketing efforts. View our Privacy Pprivacy poprivacy policy for more information.

It’s frustrating to see transactions sit in a “pending” state after making a purchase.

“I swiped my card, what more do they need to clear the funds?”

That’s why real-time payments (RTPs) are changing how we think about account-to-account money movement between financial institutions, businesses, and consumers.

Real-time payments enable near-instant transactions, something that’s long been impossible with traditional credit, debit, or even digital payments. And this new global method of money movement is catching on fast, transacting $42 billion in the first quarter of 2024 in the US.

Source: The Clearing House

RTPs enable money to move instantly, something that’s long been impossible for traditional credit, debit, or even digital payments.

__________________

What's in this post?

What are real-time payments?

How real-time payments work

Real-time payment networks

Benefits of real-time payments

How real-time payments are used today

The future role of real-time payments

Real-time payments with Aeropay x Cross River

__________________

What are real-time payments?

Real-time payments (RTPs), or “immediate payments”, allow consumers and businesses to immediately move digital funds from their bank account and receive or access money sent to them in an instant.

In the US, instant payments began with The Clearing House’s RTP® system, which currently conducts more than 60 million transactions each quarter. Now, according to a report by ACI Worldwide and Global Data, real-time payments are projected to grow 63% annually.

Learn more about real-time payments in this 1-minute video overview from The Clearing House.

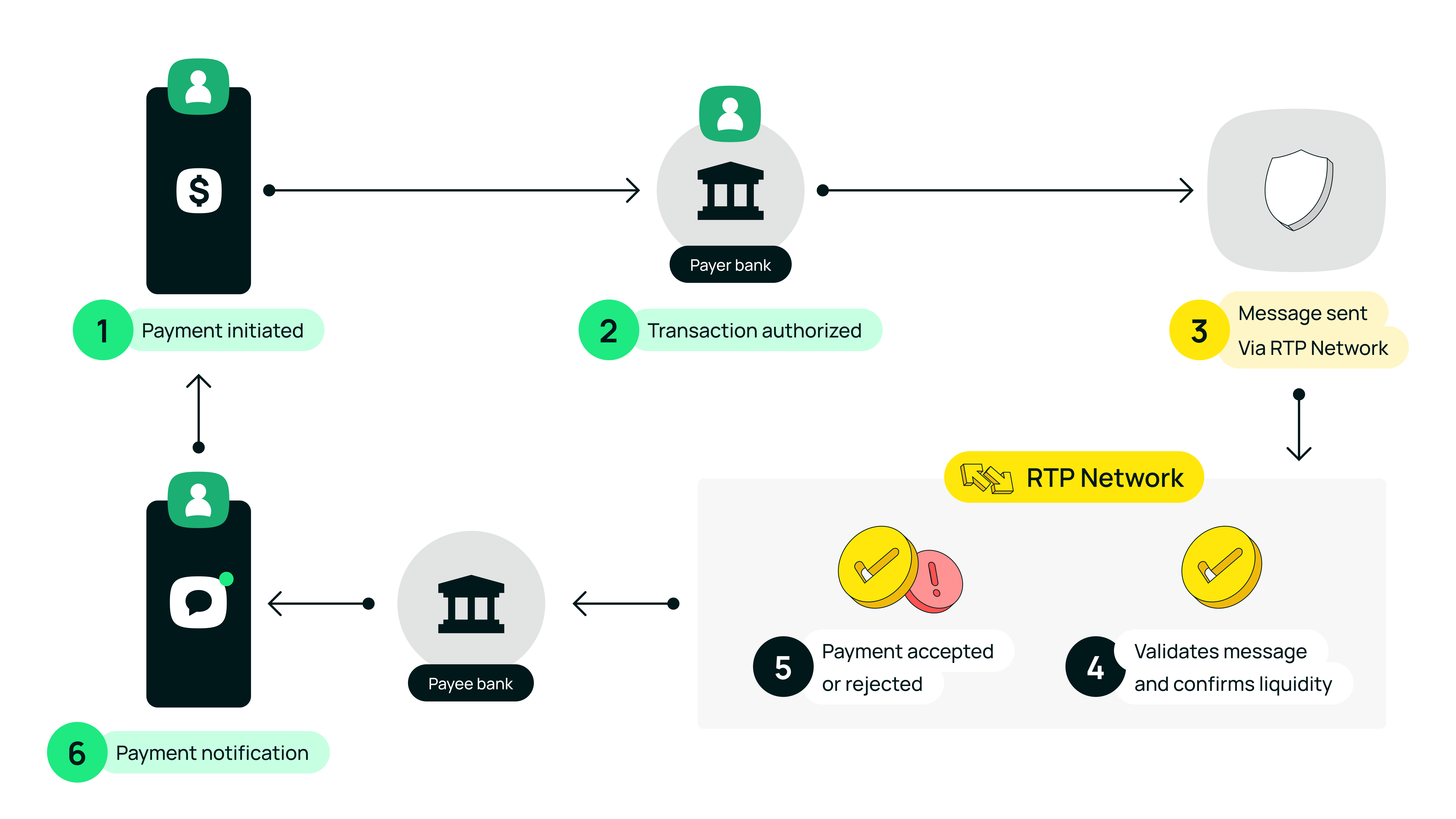

How real-time payments work

Initiation: The process begins when a payer (sender) initiates a payment transaction through their bank or a payment service provider. This can be done via online banking, mobile banking apps, or other digital platforms.

Authorization: The payer's bank verifies the payment request and checks if the payer has sufficient funds or credit to cover the transaction. Once authorized, the bank reserves the necessary amount for the payment.

Processing: The payment request is then sent to a payment gateway or clearing system, which acts as an intermediary between the payer's bank and the payee's (receiver's) bank.

Routing: The payment message is routed to the payee's bank, which also verifies the transaction details and ensures the account information is correct.

Settlement: Once the transaction is verified and approved by both banks, the funds are immediately transferred from the payer's account to the payee's account. This transfer of funds is typically completed within seconds or minutes, hence the term "real-time payments."

Notification: Both the payer and the payee receive instant notifications confirming the completion of the transaction.

Real-time payment networks

Real-time payments are part of a global pay by bank phenomenon. Still, every country has nuanced banking laws, regulations, and economic needs. That’s why there are a variety of country-based service providers for instant funds transfers.

Today, more than 56 nations have enabled instant payments on various payment rails. Here are some examples:

Faster Payment System (UK)

The Faster Payment System (FPS) in the United Kingdom was launched in 2008. It’s often cited as one of the first major real-time payment systems. The service facilitates real-time payments which are primarily initiated online, mobile, or via telephone banking for millions of individuals, businesses, and charities across the UK.

Immediate Payment Service (India)

Launched in November, 2010 by the National Payments Corporation of India, Immediate Payment Service (IMPS) offers an instant, 24X7, bank transfer service.

In 2023, India accounted for almost half of all real-time transactions worldwide, at more than 129 billion.

The Clearing House (US)

RTP® from The Clearing House is a real-time payments platform that all federally insured U.S. depository institutions are eligible to use for payments innovation. With mobile technology and digital commerce driving the need for safer and faster payments in the U.S., financial institutions of all sizes are taking advantage of the RTP network’s capabilities to create or enhance digital services for their corporate and retail customers.

FedNow (US)

The Federal Reserve launched an instant payment solution called FedNow® in July 2023.

Through financial institutions participating in the FedNow Service, businesses and individuals can send and receive instant payments in real time, around the clock, every day of the year. Financial institutions and their service providers can use the service to provide innovative instant payment services to customers, and recipients will have full access to funds immediately, allowing for greater financial flexibility when making time-sensitive payments.

Benefits of real-time payments

Real-time payments offer a host of payment optimization benefits for both merchants and consumers.

For merchants:

Improved cash flow. The immediate nature of real-time fund transfers gives large and small businesses access to money in seconds. With improved cash flow, a business has liquidity to quickly reinvest in supplies, repairs, bill payments, etc.

Enhanced security. Because RTPs occur in real-time, risk is reduced when it comes to fraud or errors. In a report from PYMNTS and TCH, Comparing and Contrasting FedNow and the RTP® Network, it’s found that 40% of real estate firms cite high security as a key consideration for RTPs.

24/7/365 availability. RTPs aren’t constrained by traditional banking daily hours or days of the week. While traditional payment methods often won’t process on the weekend or after-hours, real-time payments can be sent or received anytime.

Robust data. Real-time transactions provide considerably more data than a traditional payment. This may include invoice information, order numbers, and more. PYMNTS and TCH found 28% of firms making payments and nearly 45% of those receiving payments cite ease of tracking payments for wanting to use real-time payments. This also helps with operational efficiency as there is less time and effort spent tracking down transaction data.

For consumers:

Faster purchases. The process for real-time payments makes it easier and faster for consumers to make a purchase. Modern technology like scanning QR codes means there’s no need to carry cumbersome debit or credit cards and enhances the overall customer experience.

Instant payouts. This is especially beneficial for consumers seeking cash back, rewards, or refunds on an electronic payment. It’s also incredibly convenient for gig workers who sometimes have to wait weeks for payment.

Peace of mind. RTPs send a confirmation message immediately following the transaction, so consumers get peace of mind about exactly how much they’re charged. The simplified flow of money means they’re not waiting for a transaction to hit their account or suddenly surprised when a payment is settled days later.

How real-time payments are used today

Real-time payments have several impactful use cases in today’s industries. Some examples include:

Online gaming. Online gaming players can instantly fund their accounts and get instant payouts when they win. Learn more.

Retail. Traditional retail businesses can add RTPs for both online and in-store transactions. The instant payments make processes faster, more efficient, and safer for customers.

Gig workers. Instead of the old way of sending a request for payment and waiting weeks to be paid out, gig employees can access their earnings when needed. This new payment infrastructure opens up the gig economy and enables workers to work and get paid on their own terms.

Digital wallet transfers. Instantly move funds from digital wallets to bank accounts.

The future role of real-time payments

Real-time payments will continue gaining popularity and functionality, they will play a particularly important role in national and global financial inclusion. Global real-time transactions are expected to hit 575 billion by 2028. RTPs will have a considerable involvement in the lives and initiatives of virtually everyone.

Some examples of applications for RTPs in the near future include:

Government. RTPs can enable instant local government constituent payments for various transactions, such as tax refunds, unemployment, and social program payments.

Ecommerce. RTPs are already shaking up how consumers and businesses conduct online payments. By enabling customers to connect their bank accounts directly, businesses can accept one-click payments going forward. This simplifies the new payment process and lowers the barrier for transactions being conducted online.

Replacement of checks. The use of checks in the US is still relatively high in B2B transactions, accounting for more than 50% of overall transaction value, according to Mastercard. RTPs offer the speed and security to replace any need for checks. As more businesses realize the value, more will move away from traditional checks.

Accelerating open banking. Open banking is already accelerating a shift in money movement. Open banking payments build on existing momentum to provide real-time value to consumers and merchants.

It's only a matter of time before RTPs become the norm. There are already hundreds of participating banks in the US, and that number is growing quickly.

We’ll see much more innovation with RTPs in 2024 and beyond, especially as more banks and merchants get on board.

With a focus on transaction compliance and state-by-state regulatory approval, Cross River and Aeropay utilize custom API integrations to seamlessly onboard operators and give end users access to instant payouts, while providing security through real-time transaction monitoring.

Aeropay's partnership with Cross River offers merchants:

Real-time settlement of funds. RTP provides settlement of funds within seconds after business hours, on weekends, during holidays, and any time in between.

Real-time cash flow. Leverage Cross River’s subledgers to manage your customers on an individual basis, providing them with the visibility they need to take advantage of RTP.

Real-time risk assessment. Aeropay's continuous monitoring to detect and respond to suspicious activity in real time is paired with Cross River's APIs to mitigate fraud, chargebacks, and risk.

Real-time transaction allowances. With a transaction limit of $1M per transaction, the RTP payment rail allows you to send and receive more funds with less friction.

Real-time payouts. Send payouts instantly to user bank accounts for cash rewards or withdrawals from your platform.

To learn more about Aeropay's real-time payment offerings, schedule a demo.

%2525201.png)

.png)

.png)

.png)

%2525201.png)