How Open Banking Payments are Reinventing Money Movement in the United States

Payments

September 19, 2024

|

Nick Rudy

Open banking is revolutionizing the way we think about money movement and financial management. Learn how it will impact payments in the United States.

___________

By unlocking consumer bank data—open banking offers businesses better payment optimization.

Within this financial revolution, new forms of payment are emerging and thriving.

Open banking payments are fast, simple, secure, and affordable. And they’re disrupting the payment processing industry.

This post explains open banking payments to help you understand what they are, why they’re important, and what’s next for the money movement ecosystem.

Open banking is a financial model where consumer banking, transaction, and other financial data is opened for access to third-party providers (TPPs) via application programming interfaces (APIs).

With consent, customer data securely moves from banks and non-bank financial institutions to TPPs that layer on financial enhancements or initiate payments directly from the account.

Open banking is not a single financial product or service, but rather a system which financial services are built upon.

Open banking is important because it follows the trajectory of payments both in the US and overseas in places like European nations (Payment Services Directive - PSD2). It’s the future.

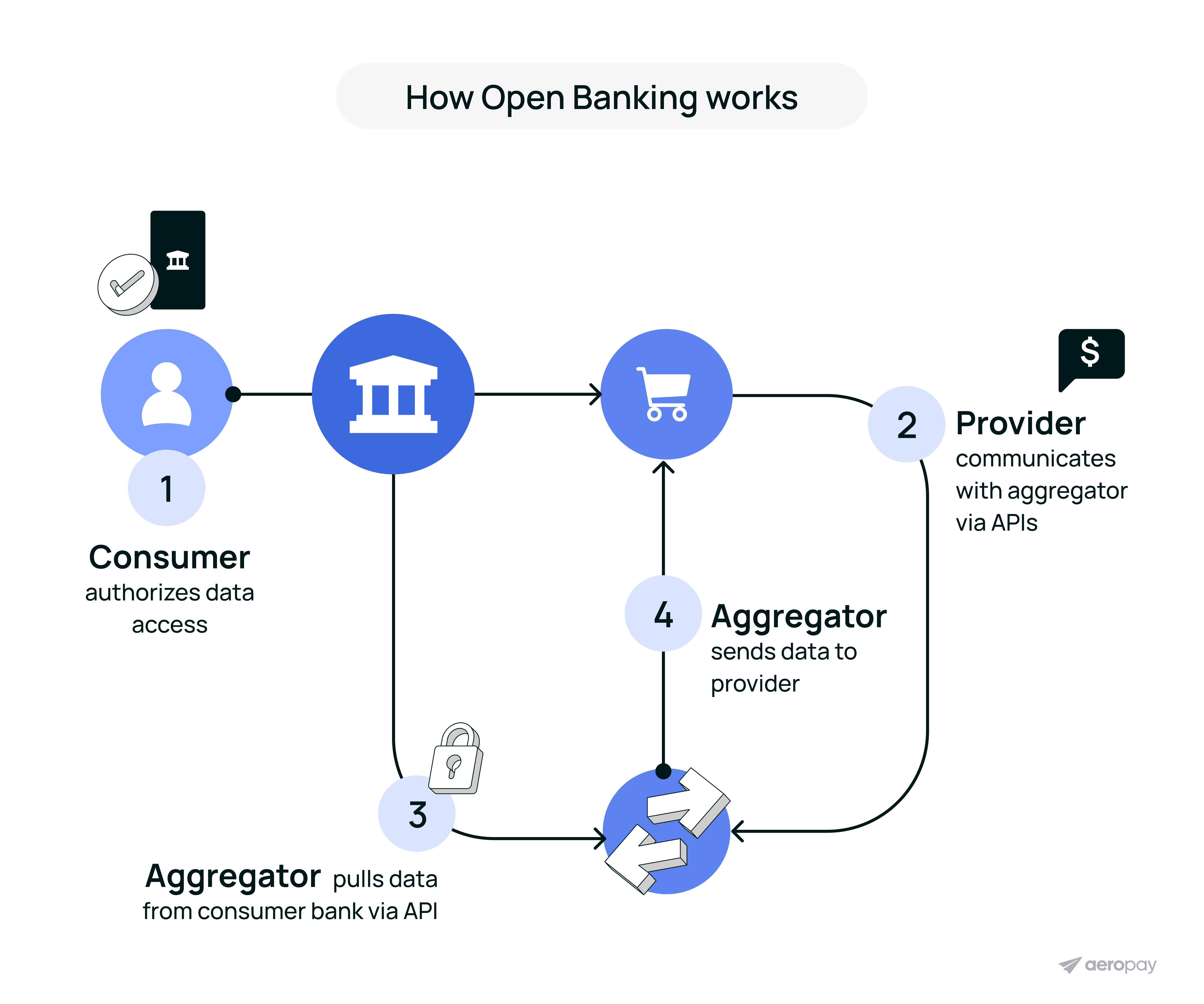

Open banking payments move money between bank accounts using APIs to authorize and initiate the transfers. This process is also called account-to-account (A2A) payments.

By linking business and customer bank accounts via APIs, financial service providers are able to layer on advancements that make open banking payments faster, more secure, and even cheaper to process than any other payment option.

Open banking payments are transferred from one bank account to another, often bypassing traditional payment intermediaries.

These payments are enabled by a third-party provider, like Aeropay, which establishes a secure connection between consumer bank accounts and merchants via open banking APIs.

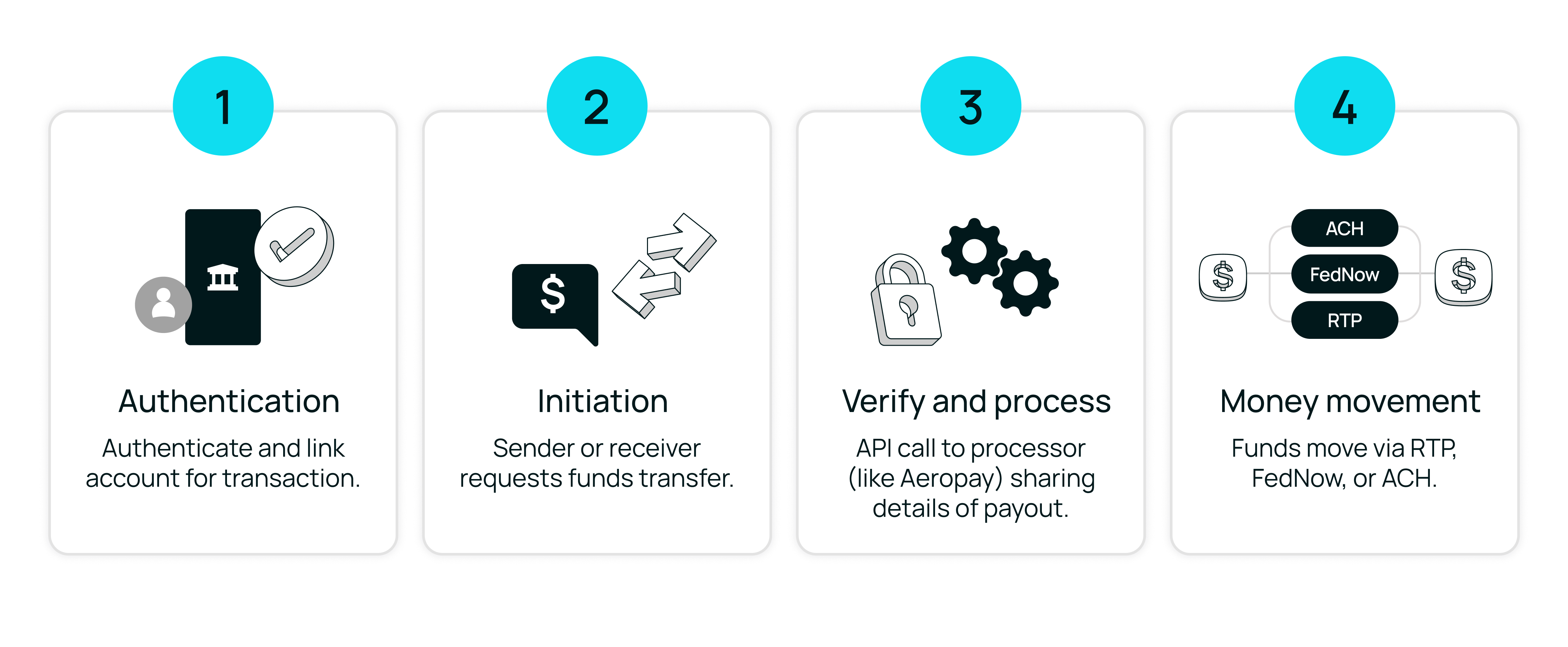

The process looks like this:

In the United States, open banking payments are already used by 36% of consumers for use cases like:

1. Recurring payments. Once authorized, consumer payments for subscriptions, rent, or utility bills can be set for auto payment via bank transfer — offering a low cost, fast processing alternative to debit or credit.

Example: Property management companies can leverage open banking payments to collect rent payments more effectively, with better financial insights. Learn about ACH rent payments.

2. Instant payouts. Real-time payouts can be sent from businesses to consumers for rewards, refunds, invoice payouts, pensions, or withdrawals from their platform.

Example: Daily Fantasy Sports operator, Dabble, uses instant payouts to allow their players to withdraw funds immediately, even on weekends or holidays.

3. Guaranteed payments. Some pay-by-bank providers shoulder the risk of returned payments by guaranteeing funds will be delivered.

Example: Utilities companies can guarantee funds will be delivered in full every month.

4. Real-time fraud detection. Open banking services unlock continuous monitoring to detect and respond to suspicious activity in real time and are paired with open APIs to prevent fraud, chargebacks, and risk.

Example: Aeroapy was able to reduce potential fraud 400% for online gaming operators during last NFL season.

Open banking payments are rising in popularity in the US because they’re a simple solution to traditionally complex and expensive payments.

The key benefits of open banking payments include:

Direct bank-to-bank transfers eliminate the need for intermediaries like card networks and payment processors, speeding up the payment process.

Open banking payments can also utilize real-time payment networks, a process that started with the launch of RTP by The Clearing House in 2017 and was followed by The Federal Reserve’s launch of FedNow in 2023.

FedNow already holds ambitious plans to attract up to about 8,000 financial institutions in the near future. As more banks come on board with open banking thanks to rule 1033, set forward by the Consumer Financial Protection Bureau (CFPB), there will be a domino effect of adoption.

When consumers choose pay-by-bank, merchants avoid interchange fees, significantly lowering transaction fees compared to traditional credit, debit cards or even digital wallets. This is the biggest advantage of A2A payments.

In 2023, US merchants paid $101 billion in Visa and MasterCard credit card processing fees, including $72 billion in interchange fees. Most merchants are paying a hefty 2-5% fee for each credit card payment — and that number’s been increasing.

Open banking payment fees are much lower. See a full cost comparison here.

.png)

Open banking ensures transparent data control between financial institutions, merchants, and third-parties. Merchants can access real-time bank account data directly from consumers’ banks, which enhances the authentication process and reduces the risk of fraud.

Businesses are also able to easily verify account information, such as account balance, which ensures funds are available before completing a transaction.

At the same time, merchants can set up effective processes to limit fraudulent transactions, alongside typical processor risk mitigation practices like bank-level authentication and passwordless authentication, which verifies a user in seconds using their device's face or touch ID. .

Open banking solutions like Aeropay leverage a smart fraud engine that is selective about what transactions get let through, while still maintaining a high acceptance rate.

Open banking regulations establish standardized protocols for data sharing and payments, ensuring a level playing field for all market participants.

At the same time, regulatory frameworks protect consumer data and ensure security for the end user experience.

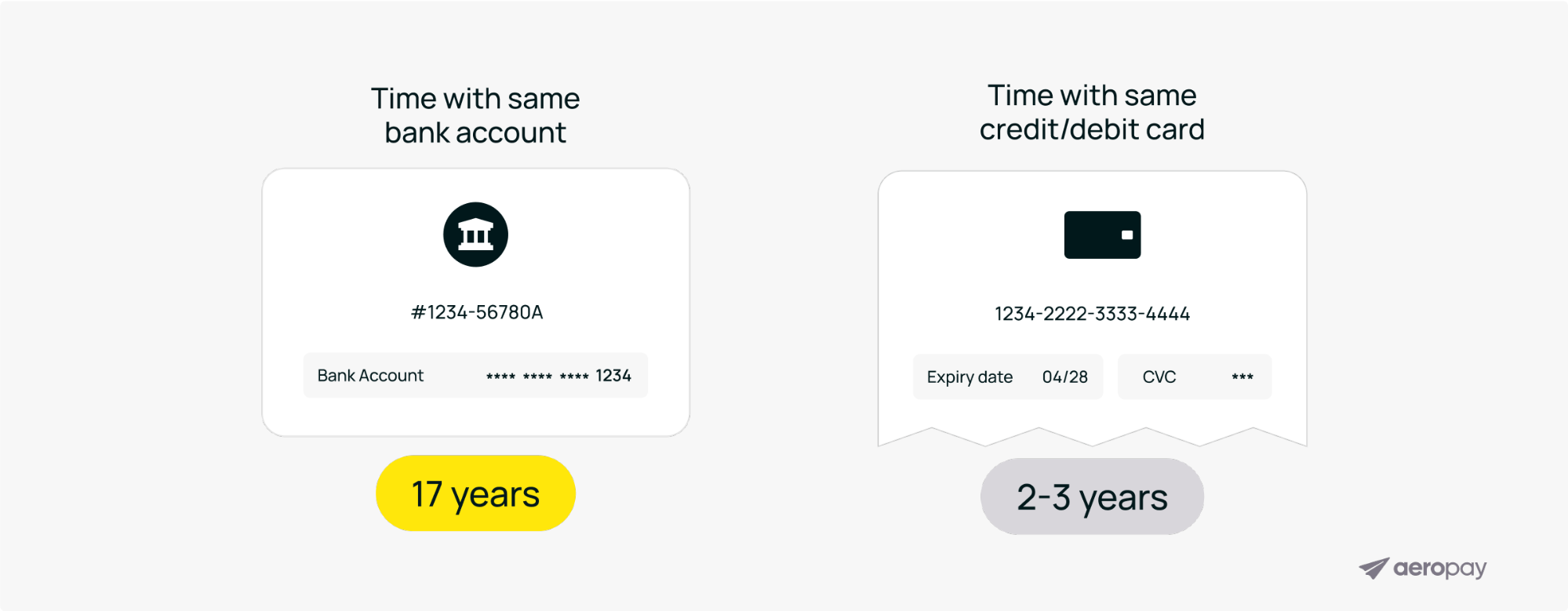

Traditional cards expire every three years on average. And many consumers lose or replace them even sooner.

On the other hand, US adults use the same primary checking account for more than 17 years on average.

For subscriptions, bill payments, or more reliable e-commerce account transactions, there’s immense value in durable financial information to reduce payment churn and minimize chargebacks.

Consumers don’t have to add new card details every time they’re updated. Instead, a single bank link connects an account for every future transaction.

Build a deeply embedded payment experience with solutions like Aeropay’s Payment API. Enable one-click checkout and provide a unique and seamless customer experience.

Consumers don’t have to add new card details every time they’re updated. Instead, a single bank link connects an account for every future transaction.

The way consumers pay hasn’t evolved much in the past couple decades—but that’s changing.

New financial technology (fintech) in the payments landscape like NFC and mobile wallets are catching on fast, but there’s a more significant payments revolution bubbling to the surface—and it’s sparked by open banking.

Open banking payments are fast, affordable, secure, convenient because they directly transfer funds from one bank to another.

Cards can’t keep up as their transactions are processed through payment networks like Visa or MasterCard, involving multiple intermediaries such as acquiring banks, issuing banks, and card networks.

Aeropay CTO Josh Lockhart explains the rising account-to-account model as an “ability to strip away the fluff from cards, lean on the strengths of banking, and facilitate a simpler money movement concept that’s actually more convenient.”

We’re entering a new era of money movement and financial inclusion. Traditional payment methods now face heavy competition from open banking payment solutions. As consumers and merchants further adopt open banking payments, disruption will increase exponentially.

Aeropay's payments-first platform seamlessly connects bank accounts and processes open banking payments. We’ve built our own bank-linking technology, called Aerosync, that’s customizable and built to scale with your business.

Aeropay enables customizable integrations via a full suite of open APIs. The commercial impact for your business is significant, with industry-leading approval rates, low returns and fraud, and exceedingly high conversion rates.

Contact our open banking payments experts to see how Aeropay can help your business.