Guaranteed ACH: What it is and why it matters for your business

Payments

May 21, 2026

|

Nick Rudy

There were 8.9 billion ACH transfers processed in the first quarter of 2026, according to Nacha. ACH volume continues to grow as businesses continue to move volume toward cost-effective bank rails.

But there is still one persistent gap in ACH performance: the time delay between the moment a payment occurs and the moment it settles.

Settlement delays cause ACH payments to carry a higher return risk for reasons such as insufficient funds, invalid accounts, fraud, or disputes. This creates operational and financial risk for businesses that need to release products, provide services, or make funds available before settlement is finalized.

Guaranteed ACH solves this problem by protecting businesses from the financial risk of returned or failed ACH payments. Instead of the merchant absorbing the loss, the guarantee provider assumes the return risk so businesses can accept bank payments and release funds, products, or services with confidence.

This article explains what Guaranteed ACH is, how it works, and why it has become an important solution for businesses looking to scale bank payments without taking on traditional ACH settlement risk.

Before we cover guaranteed ACH, it’s important to understand how ACH payments work and why they often carry higher risk.

The Automated Clearing House (ACH) network is the primary system used to move money directly between bank accounts in the United States. Managed by Nacha and operated through the Federal Reserve and private ACH operators, the ACH network powers billions of transactions each year, including direct deposit, payroll, bill payments, tax refunds, recurring payments, and bank-to-bank transfers.

When a consumer initiates an ACH payment, funds do not move instantly. Instead, transactions are submitted in batches between financial institutions through the ACH network. The originating depository financial institution (ODFI) sends the transaction to an ACH operator, which then routes it to the receiving depository financial institution (RDFI) responsible for the recipient’s bank account.

Because ACH transactions move through scheduled settlement windows, standard ACH processing can take 1-3 business days to fully settle. This delay is one reason ACH payments have traditionally been slower than card payments or real-time payment methods.

Same Day ACH was introduced to improve processing times by allowing eligible ACH payments to settle faster during designated windows throughout the day. While Same Day ACH significantly reduces settlement delays, it still depends on banking hours, cutoff windows, weekends, and Federal Reserve processing schedules. As a result, ACH payments still do not settle instantly in many scenarios, especially outside standard business hours.

These settlement delays create risk for businesses. Even if an ACH payment initially appears approved, the transaction can still later return due to insufficient funds, invalid account information, disputes, or fraud. These ACH returns create operational overhead, increase payment risk, and make it difficult for businesses to confidently release products, services, payouts, or funds before settlement finalizes.

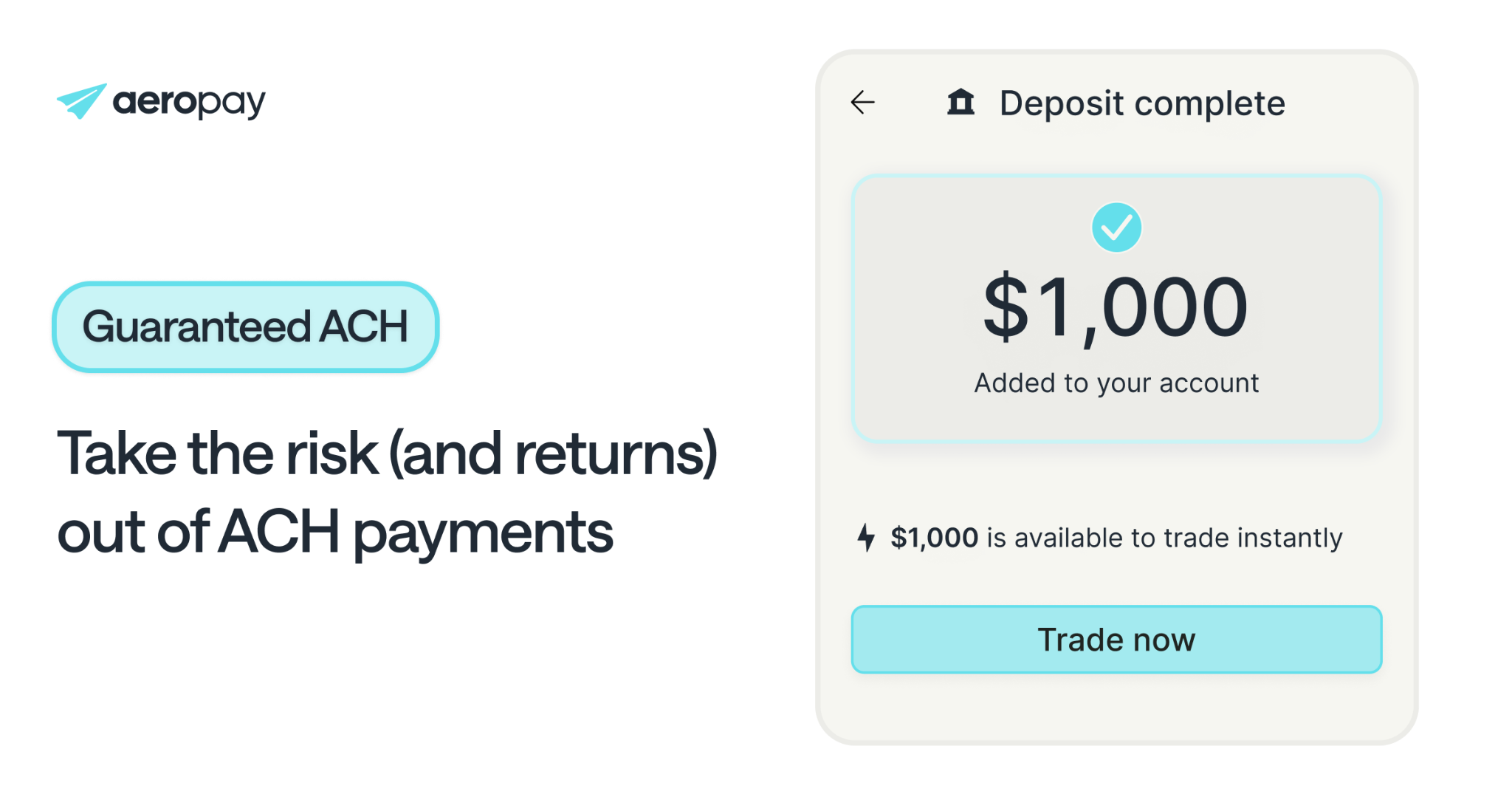

Guaranteed ACH protects businesses from the financial risk of returned or failed ACH payments.

Instead of the merchant absorbing the loss when a bank payment fails, the guarantee provider assumes the return risk and ensures approved transactions are covered. This gives businesses the confidence to accept ACH payments and release products, services, or funds before settlement completes.

What makes this possible is modern pay by bank technology. By securely connecting consumer financial accounts in real time, providers can analyze account balances, transaction history, and other risk signals to more accurately predict ACH return risk before funds move.

As a result, businesses can scale low-cost bank payments without taking on the uncertainty traditionally associated with ACH settlement.

Guaranteed ACH payments work by combining bank connectivity, account intelligence, and predictive risk models to evaluate ACH transactions before settlement occurs.

The process typically looks like this:

The risk analysis under the hood is highly sophisticated, but from the outside, it’s just a fast, seamless payment.

Guaranteed ACH allows businesses to scale lower-cost bank payments without taking on the uncertainty traditionally associated with ACH settlement.

This is especially important for businesses that need to deliver real-time customer experiences, where products, services, or funds must be made available before ACH settlement completes.

Benefits of guaranteed ACH payments include:

Businesses can confidently release products, services, trading balances, gameplay, and other real-time experiences without waiting days for ACH settlement.

The guarantee provider assumes the financial risk of approved ACH transactions, protecting businesses from returned or failed payments.

Because ACH return risk is covered, businesses can approve more legitimate customers without increasing financial exposure. This helps reduce unnecessary declines and convert more payment attempts into completed transactions.

Guaranteed ACH removes much of the operational burden associated with managing ACH risk internally, including manual reviews, payment recovery workflows, return monitoring, collections efforts, and ACH reconciliation.

ACH payments typically cost significantly less than debit and credit card transactions, helping businesses improve payment efficiency and margins.

Not all guaranteed payment systems are created equal. Many payment solutions use the term, but what’s actually covered (and how well) can vary a lot.

Some providers only cover certain return codes or place strict conditions on what qualifies for coverage. Others quietly lower approval rates substantially in order to reduce their own financial exposure, creating friction for legitimate customers and limiting payment conversion.

The effectiveness of guaranteed ACH also depends heavily on the provider’s underlying payment infrastructure and risk models. Providers with limited transaction history or isolated merchant data often struggle to accurately predict ACH return risk at scale.

Effective guaranteed ACH requires more than basic risk scoring. It requires direct bank connectivity, network-level intelligence, real transaction outcome data, and years of operational ACH expertise to accurately approve good payments while minimizing financial risk.

Businesses evaluating guaranteed payment processors should also understand approval thresholds, coverage limitations, pricing, and how each provider evaluates customer account risk.

Aeropay has spent more than a decade building guaranteed ACH infrastructure designed specifically for modern bank payments.

Aeropay’s platform combines API-based bank connectivity, real-time account intelligence, network transaction data, and AI-powered risk models to accurately predict ACH return risk and approve more legitimate transactions.

Aeropay’s Guaranteed ACH solution helps businesses:

Today, Aeropay supports millions of connected bank accounts and powers Guaranteed ACH payments across industries like gaming, fintech, trading, wellness, and bill payments.